Asian biomethanol is pricing below Europe biomethanol, a gap that could widen as lower-carbon marine fuel compliance demand shifts east.

FuelEU Maritime rules allow certified low-carbon fuels bunkered outside the EU to count toward compliance, but Europe's anti-dumping duties have raised the cost of Chinese biodiesel imports. The result is compliance arbitrage: shipowners can "mass-balance" biomethanol bought in Asia into their EU voyages, meaning they can use certificates proving equivalent Asian supply instead of physically bunkering in Europe. The result is that Chinese and Singaporean prices — and not those in Rotterdam — are setting the global benchmark.

The pace of this pricing change becomes clearer when looking back only a few months. On 5 May, Shanghai Port conducted its second commercial biomethanol bunkering: 3,110t for HMM's methanol-capable vessel [HMM Forest](http://direct.argusmedia.com/newsandanalysis/article/2685236), following its first 2,902t delivery on 30 March. In July 2025, Towngas delivered 5,000t of ISCC-EU certified biomethanol via Tianjin to Singapore for bunkering trials, proving large-scale certified supply chains are viable. Shanghai Electric also started up a new ISCC-EU certified plant in Jilin province in July, explicitly targeting marine bunkering.

More supply is also coming online in Asia. [Goldwind Green Energy]( http://direct.argusmedia.com/newsandanalysis/article/2721473) plans to commission a 250,000 t/yr hybrid bio/e-methanol project in Inner Mongolia, in September 2025, with long-term offtake agreements already signed with Maersk (500,000 t/yr) and Hapag-Lloyd (250,000 t/yr). CIMC Enric will start trial runs at its 50,000 t/yr biomethanol plant in Guangdong this autumn, ramping up to 250,000 t/yr by 2027.

Prices reflect this eastward anchor.

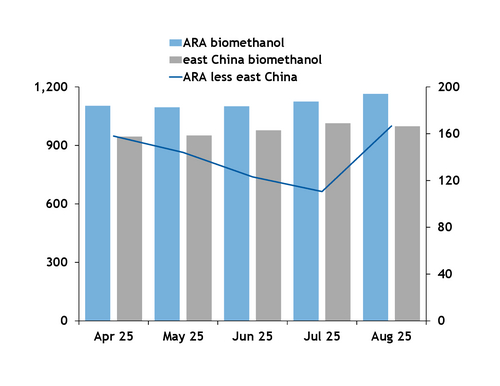

In August, Argus assessed east China dob biomethanol at $1,000/t compared with $1,164.60/t at the Amsterdam-Rotterdam-Antwerp hub (see chart). With FuelEU accepting certified bunkering outside Europe, shipowners can mass-balance cheaper Chinese or Singaporean biomethanol into EU voyages, bypassing Europe's higher biodiesel and e-methanol premiums.

European policy is amplifying the shift. Anti-dumping duties on Chinese biodiesel, ranging from 10-35pc, raise EU biofuel costs. Meanwhile, EU regulators have confirmed that certified fuels bunkered abroad can count toward FuelEU compliance, provided documentation is intact. That combination encourages owners to source in Asia, where supply is growing and prices are lower.

Risks remain. The EU is already tightening scrutiny of certification systems after fraud allegations in Chinese biofuels, and future reforms could restrict book-and-claim mass balancing. Industry groups also warn that the Union Database for Biofuels could impose costly fees, tight deadlines, and double-counting risks, potentially affecting biomethanol development.

But the trajectory is unmistakable. Argus tracks a pipeline of nearly 42.5mn t of low-carbon methanol capacity by 2030, much of it in China. China alone has announced 72 biomethanol and e-methanol projects (15mn t/yr), with 24 projects (3.2mn t/yr) under construction or at FID stage.

Singapore is also moving fast. Its Maritime and Port Authority announced a new methanol bunkering standard in March and opened methanol bunkering license applications. The five-year license, valid from 1 January 2026 to 31 December 2030, will be awarded in the fourth quarter to firms that meet safety and operational standards.

Demand is rising in tandem. As of August 2025, more than 60 methanol-capable vessels are in operation, with another 300 on order.

Until Europe scales its own production or tightens FuelEU rules, biomethanol prices, and compliance costs, will increasingly be set in Asia, not in the EU.