France's underground gas storage sites are heavily depleted following a fast stockdraw recently, and there may be limited potential for injections to start in March.

French withdrawals have held above 1TWh for each day since 25 December, except for 15-19 and 25-26 January when milder spells reduced the stockdraw. The net stockdraw of 1.22 TWh/d on 1-26 January was well above the three-year average of 986 GWh/d.

French stocks were at 41.1TWh — or 33pc of capacity — this morning, six percentage points lower than a year earlier. Inventories are on track to enter February at their lowest since the 38TWh in 2022.

If withdrawals maintain the same pace as on 1-26 January, France would enter February with 35TWh in storage. But if withdrawals fall back to the three-year average pace — given milder weather forecasts — this would leave 36.3TWh in storage on 1 February.

And if firms maintain withdrawals at the rate of 822 GWh/d in February — in line with the three-year average — the country's stocks could enter March at 11.9-13.3TWh, limiting the flexibility for fast withdrawals in March.

While firms typically start injections before April, near-curve prices suggest an incentive for firms to maintain withdrawals over the month this year.

French net storage injections started before 1 April in all but one of the past four years — the first day of net injections was on 20 March last year, 29 March the year before that and as early as 11 March in 2022. Injections started later than normal at 7 April in 2023.

The Peg March price closed €2.06/MWh below the February contract on Monday, but remained €4.90/MWh above the April price. And the Peg summer 2026-winter 2026-27 spread closed at +€1.16/MWh, making summer injections unprofitable.

But French storage products came with filling targets for October, which may prompt firms to inject in summer despite unfavourable spreads. The first target applicable is 20pc at the Sediane Nord site by 31 May. And all products marketed by Terega and Storengy have a minimum fill of 85pc by 31 October (see table).

Potential for Mar withdrawals

Firms may need to maintain withdrawals in March to sustain strong exports to neighbouring markets, even if LNG imports are as high as preliminary schedules suggest.

Market participants have booked 22 unloading lots for March across the three Elengy-operated LNG facilities. But firms often shift their slot bookings closer to the delivery period depending on demand and price incentives.

Average cargo sizes in 2025 were roughly 1.05TWh at Montoir, 887GWh at Fos Cavaou and 561GWh at Fos Tonkin. If March unloadings at the Elengy terminals match those averages, a combined 21TWh of LNG would be delivered, enough to support 677 GWh/d of sendout if spread evenly across the month.

And the latest forward plan for Dunkirk, based on available slots and cargo sizes estimated by capacity holders, showed total estimated monthly unloadings reaching 14.45TWh in March, enough to sustain 466 GWh/d of sendout.

French demand normally steps down in March from January-February. The French state weather agency, in its three-month outlook published on Monday, attributed a 50pc likelihood that February-April temperatures will hold above seasonal norms, and a 30pc likelihood of weather in line with the long-term averages.

Assuming March demand is approximately 1.25 TWh/d — in line with this month in 2024, when overnight lows in Paris were 1°C above seasonal norms — regasification could meet about 93pc of the country's demand.

But if firms maintain strong net exports, then withdrawals may need to continue even if domestic consumption is weak. And forward prices suggest that firms may continue to export towards Italy at near capacity and will ship gas to Belgium, but that there will be some inflows from Spain.

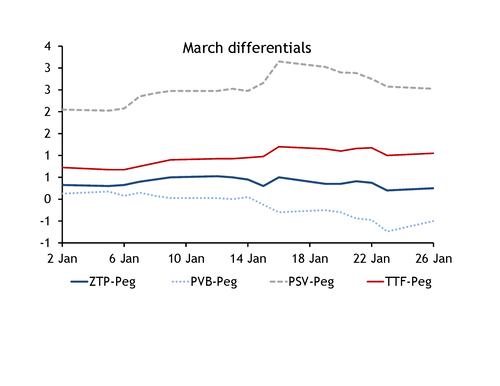

The Peg March market closed €2.525/MWh below the Italian PSV on Monday, suggesting an incentive for firms to maximise exports at Oltingue towards Italy. And the Peg March contract closed €0.25/MWh below the Belgian ZTP and €3.21/MWh below Germany's THE, suggesting that exports to Belgium will continue. Much of the gas arriving in Belgium recently has been transited on to Germany and the Netherlands.

France has been a strong net exporter at 280 GWh/d so far this month. The country has in recent years been a net importer in March.

| Minimum fill levels by product | % | ||||

| Site/product | Technical capacity | 31 May | 31 Jul | 31 Aug | 31 Oct |

| Saline | 11.7TWh | 85 | |||

| Sediane Nord | 16.7TWh | 20 | 50 | 85 | |

| Sediane B | 10TWh | 85 | |||

| Serene Atlantique | 48.2TWh | 85 | |||

| Lussagnet (Fair) | 33.9TWh | 30 | 85 | ||

| Lussagnet (Fast) | 85 | ||||

| Lussagnet (Fizz) | 30 | 85 | |||

| Lussagnet (Opstock) | 85 | ||||

| — Storengy and Terega | |||||