Slovakia is likely to end the heating season with record-low gas inventories, potentially forcing the country to more than double summer imports to support injections.

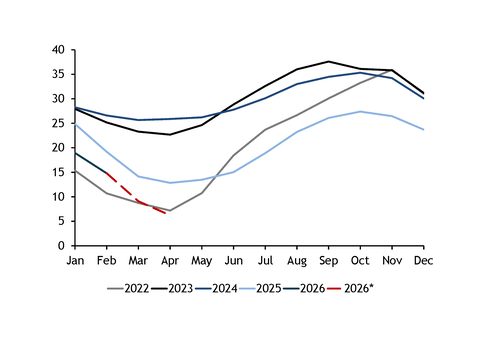

Slovak storage withdrawals have intensified this winter. Inventories fell to 13.7TWh on Monday morning, or 37pc of capacity, at a 7.1TWh year-on-year deficit (see Slovak stocks graph). This excludes the 6.9TWh Dolni Bojanovice storage site that is located in the Czech Republic but is connected to Czech and Slovak gas grids. Dolni Bojanovice held 5.4TWh on Monday morning and was 77.5pc full.

Assuming net withdrawals from sites located in Slovakia over the rest of the winter will hold at 147 GWh/d or 3pc above last year's rate — same as so far in the season — Slovak stocks could drop to about 6.4TWh, or 17pc of capacity, by the end of March. This would be down from 13TWh a year earlier and the lowest level for that date since 2022.

Such a low starting point would sharply increase summer injection needs. Slovakia would need to more than double its injection pace compared with summer 2025, requiring about 26.6TWh of cumulative injections in April-September, roughly 12.7TWh more than last summer to reach a storage level of 33TWh by 1 October — the three-year average for the day in 2023-25.

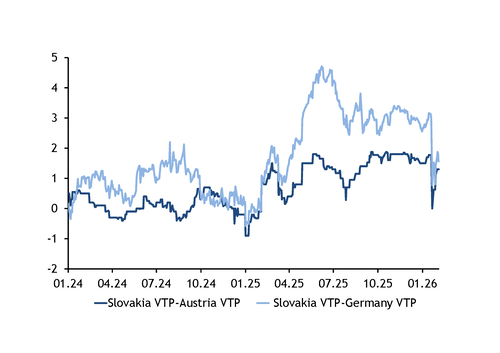

This is likely to increase competition for flexible summer volumes in landlocked central European countries where stocks are also likely to end winter at a multi-year low. Slovak prices have largely held at a premium to neighbouring markets in recent months, but demand for additional supply could potentially widen regional price differentials further, especially in peak injection months (see Slovak price graph summer 2025).

Slovakia's Russian gas share to fall on stronger injection needs

Slovakia's higher import requirements ahead of the 2026-27 heating season could bring an earlier drop in Russian gas in its supply mix, reducing the country's reliance before a full phase-out next year.

Slovakia's supply mix has changed since January 2025, when transit of Russian gas through Ukraine stopped, increasing imports from the west and LNG-linked routes.

State-owned supplier SPP has a 6bn m³/yr contract with Russia's Gazprom until 2034, which was partly suspended in January 2025 as a lack of an interconnection agreement at the Ukrainian-Russian border narrowed delivery options for Russian gas. But while some of the contracted volumes have been imported to Slovakia through the 15.75bn m³/yr Turkish Stream pipeline since February 2025, it forced SPP to sign diversification contracts with BP, ExxonMobil, Eni and RWE.

Flows from Hungary accounted for 65pc of Slovakia's gross imports last year, with 24pc coming from the Czech Republic and 11pc from Austria last year. The share of Hungarian deliveries was unchanged in summer, while imports from the Czech Republic made up 20pc and Austria 15pc.

Deliveries at Velke Zlievce averaged 77.4 GWh/d in April-September, 24.4 GWh/d below the technical capacity of 101.8 GWh/d in that period, although nameplate capacity rose to 127.2 GWh/d from 1 December. But capacity at the Hungarian-Serbian Kiskundorozsma 2/Horgos point has been running close to its technical limit last year, leaving no scope to increase Russian gas deliveries into the region this year.

This suggests that Russian-sourced gas remained dominant in Slovakia's supply mix, but substantially lower than in 2024 when the country received 99pc of gross imports at the border with Ukraine.

But with injection needs set to almost double this summer and limited technical capacity to receive Russian volumes, the share of Gazprom-contracted gas could fall this summer, if Slovakia wants to replenish its stocks and meet EU-mandated targets of 90pc in 1 October-1 December.

Slovakia can receive Russian gas only for the next two injection seasons because EU legislation requires a complete phase-out of Russian supply by September 2027.

The EU needs to complete strategic infrastructure in Germany and Austria and strengthen capacity along supply routes from Poland and Greece to cope with the challenges posed by the new EU legislation, Slovak economy minister Denisa Sakova said on 29 January. And costs to transport gas need to be lowered by adjusting tariff-setting methodology in EU legislation, Sakova said.