UK chemicals-sector electricity demand is falling more slowly than output and gas use, and could in future be supported by new hydrogen electrolysis load even without a recovery in traditional production.

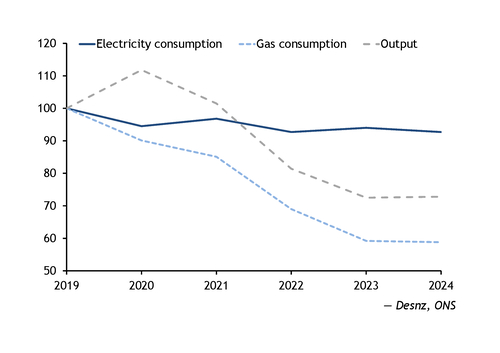

UK chemicals-sector electricity consumption was 14.7TWh in 2024, down by 7pc from 15.8TWh in 2019 before the pandemic, according to the latest data from the Department for Energy Security and Net Zero (Desnz), having fallen slowly but steadily over the period. The production for manufacture of chemicals and chemical products index fell by 27.2pc over the same period, according to data from the Office for National Statistics (ONS). This means output has fallen almost four times faster than electricity consumption, suggesting the remaining industrial base is more power-intensive (see consumption and output graph).

Natural gas consumption in the chemicals sector has aligned more closely to the fall in output, with gas demand falling by 41pc between 2019 and 2024, to 12.3TWh. That divergence between the decline in gas and electricity consumption is consistent with natural gas often functioning as both feedstock and fuel in bulk chemicals. In ammonia production, gas typically accounts for most of the production cost, leaving domestic output vulnerable when UK costs rise above import parity.

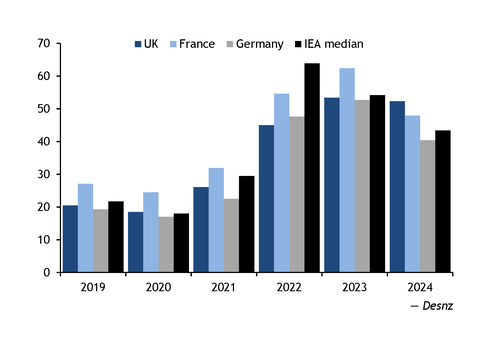

Recent closures and curtailments in some of the UK's most gas-intensive segments, including ammonia and ethylene, have resulted from higher gas prices. UK industrial natural gas prices excluding taxes rose from £20.50/MWh in 2019 to £52.30/MWh in 2024, around 20pc above the IEA median and higher than in France and Germany (see industrial gas price graph).

Remaining base more resilient

The operations that remain are the most electricity-intensive parts of the sector, with some better able to sustain power demand.

Chlor-alkali production is highly power-intensive, with rising electricity costs reducing UK output to a negligible share of European capacity. And much of that capacity is currently off line, with Ineos Inovyn at Runcorn being the sole major UK chlorine producer.

Other electricity-intensive activities that remain in the sector are tied to more diversified end markets than bulk chemicals. German firm Linde's subsidiary BOC operates seven air separation units across the UK and Ireland, serving customers in healthcare, food processing, metals and electronics — end markets broad enough to buffer sector-specific demand shocks.

"The primary factor is their ability to pass through additional cost because of the cruciality of certain industrial gases for manufacturing processes," industry association the Energy Intensive Users Group director Arjan Geveke said. "Also, the trade intensity of certain industrial gases is low," he said. Unlike ammonia or ethylene, cryogenic gases such as oxygen and argon are not widely traded internationally, limiting the import competition that has hit commodity chemical producers.

High electricity costs still weigh on the sector

UK government support schemes have so far done little to change the sector's broader cost disadvantage.

The pressure on producers reflects both structurally high input costs and weak demand. "For some chemical companies energy, as a proportion of their cost base, [is] 50, 60, 70pc," Chemical Industry Association (CIA) chief executive Stephen Elliott told Argus. Among CIA members, electricity accounted for a greater share of total energy spend than gas in 2024, despite members consuming roughly four times more gas, Elliott said.

Schemes such as the British Industry Supercharger — a UK government initiative launched in 2023 to support the competitiveness of energy-intensive industries — had provided temporary relief for some sites. But under the recently proposed British Industrial Competitiveness Scheme aimed at cutting electricity costs for manufacturers in key growth sectors, "the relief will be far outweighed by the incoming increase in policy and network costs", Elliott said. And unless the full chemicals sector is covered, costs will be redistributed to non-eligible sites. Some companies benefiting from network-charge relief under existing arrangements will mean that "it's the rest of industry that pays for the relief", he added.

Hydrogen may add some future demand

New electrolysis projects could add some load later this decade, although the effect on chemicals demand is likely to be limited.

Based on the nine active projects in the first hydrogen allocation round (HAR1), renewable hydrogen output could reach around 15,700 t/yr by the end of the decade, implying about 880 GWh/yr of electricity demand assuming electrolyser consumption of 56 kWh/kg (see HAR1 projects table).

The build-out is expected to be gradual, with one active project from HAR1 due to enter service by 2027, four by 2028 and a further four by 2029. Not all of that new load would sit within chemicals, since some projects are aimed at a broader industrial base and some at users outside chemicals altogether. MorGen Energy's 20MW Milford Haven project is intended to supply customers in the industrial, chemical and port sectors, while beyond the first allocation round, Meld Energy's proposed 100MW Saltend Green Hydrogen Hub would supply users at Saltend Chemicals Park, and EdF Hynamics' planned 120MW Fawley project is intended to supply ExxonMobil's refinery and petrochemical complex.

| HAR1 projects summary | |||||

| Project name | Developer | H2 output (MW HHV) | Implied H2 output (t/yr) | Implied electrical consumption (GWh/yr) | Long stop date |

| Active projects | 106.15 | 15,721 | 878 | ||

| Barrow Green Hydrogen | Carlton Power & Schroders Greencoat | 21.02 | 2,557 | 143 | 31 Mar 2029 |

| Bradford Low Carbon Hydrogen | Hygen Energy & N-Gen Energy | 24.49 | 4,202 | 235 | 31 Dec 2028 |

| Green Hydrogen 3 (Northfleet Green Hydrogen) | Hyro (Octopus Energy Generation) | 9.00 | 1,203 | 67 | 01 Dec 2028 |

| HyBont Bridgend Green Hydrogen | Hygen Energy | 5.20 | 687 | 38 | 29 Jun 2029 |

| HyMarnham Power | GeoPura & JG Pears | 9.30 | 1,774 | 99 | 26 May 2027 |

| Langage Green Hydrogen | Carlton Power & Schroders Greencoat | 7.01 | 850 | 48 | 31 Mar 2029 |

| Tees Green Hydrogen | Hynamics (EdF) | 5.51 | 1,059 | 59 | 31 Dec 2028 |

| Trafford Green Hydrogen | Carlton Power & Schroders Greencoat | 10.52 | 1,524 | 85 | 31 Mar 2029 |

| West Wales Hydrogen | MorGen Energy (Trafigura) | 14.10 | 1,865 | 104 | 31 Dec 2028 |

| Paused projects | 17.70 | 3,551 | 199 | ||

| Cromarty Green Hydrogen | ScottishPower & Storegga | 10.60 | 2,131 | 119 | 26 Dec 2028 |

| Whitelee Green Hydrogen | ScottishPower | 7.10 | 1,420 | 80 | 29 Dec 2028 |

| — Low Carbon Contracts Company, Argus | |||||