Stock, demand and trade data suggest the UK is the most exposed country in Europe to tightening diesel and jet fuel supply, with Denmark and Portugal also at risk.

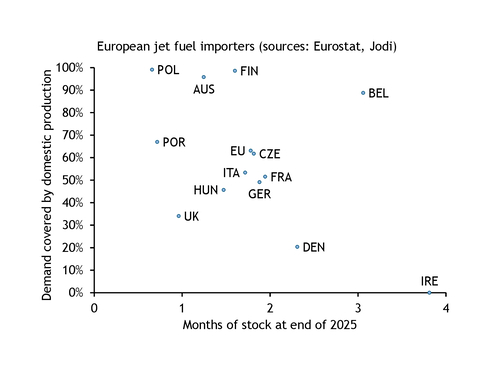

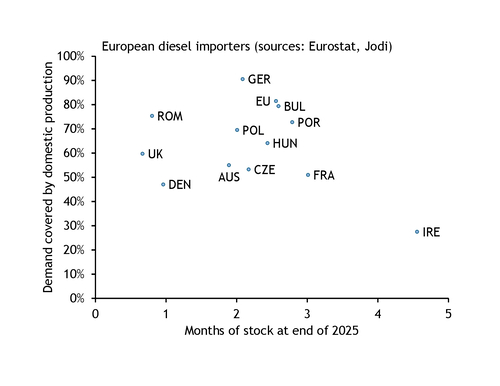

Short jet fuel (see chart 1) and diesel (see chart 2) trade balances, combined with low stock cover leave these net importers particularly vulnerable if traffic through the strait of Hormuz remains effectively closed.

Countries where production matches or exceeds consumption — such as Poland and Greece — can operate with lower stocks because they are less reliant on imports. And countries that rely on imports but hold deeper stocks, such as Ireland, are better cushioned against Mideast Gulf supply disruptions.

The assessment draws on national statistics reported to the Joint Organisations Data Initiative (Jodi) and the EU's Eurostat, combined with Argus analysis.

The conflict in the Middle East is unlikely to see any European country run out of refined oil products entirely because the war limits only part of their import supply. Even the least well-stocked countries have a few weeks of cover if they lost both domestic output and imports. But national stocks could fall to uncomfortably low levels, leading to localised shortages and sharper price swings even where overall stocks remain.

The theoretical life expectancy of national stocks offers a simple guide to the relative risk of such local shortages. If Mideast Gulf supply cannot be replaced, and if the impact spreads proportionally across importers, then the UK could exhaust kerosine stocks in three months and gasoil in nine, according to Argus calculations using Jodi data. These categories mainly represent jet fuel and road diesel.

Portugal could run out of jet fuel stocks in four months, based on Eurostat data. Hungary could run out in five months, Denmark in six, Italy and Germany in seven, and France and Ireland in eight. Refinery closures have tightened jet fuel balances across western Europe as demand has risen, while diesel balances have been less affected because demand has broadly declined.

On road diesel, Denmark could in theory deplete stocks in nine months. Romania could do so in 16 months, Austria in 21 and the Czech Republic in 23. These figures are illustrative rather than forecasts: in practice, stock life would likely converge to some extent as countries with thinner cover would bid higher for imports to slow the depletion of their inventories.

Seasonal patterns will also affect stockdraws. Stocks usually fall in spring and autumn because of refinery maintenance, and rise in summer when runs increase. But imports also fluctuate seasonally, so any major disruption could unsettle normal trends. In Portugal's case, jet fuel stocks should cover this spring because its only refinery got its maintenance work out the way last year. But Portugal usually resumes jet imports around May, mainly from the Mideast Gulf. If tanker traffic through the strait of Hormuz is still heavily restricted by then, its jet stocks could decline rapidly.

Poland holds very low jet fuel stocks but is close to self-sufficient, producing roughly what it consumes. It had less than one month of cover at the end of 2025 — the lowest among major EU states — but it need not draw stocks unless refinery issues arise or higher international prices pull product across borders. Both risks are real: Poland's two largest refineries face heavy maintenance this year, and its national balance masks the fact that it regularly imports and exports jet fuel across different borders. If those flows fall out of balance, Poland's thin stocks could drain.

Ireland is fully dependent on jet fuel imports, as its sole refinery does not produce jet. But its deep stocks — nearly four months of cover — would cushion a complete loss of supply.