High soybean oil and meal prices have driven US soybean crush margins to record levels in recent weeks, a trend likely to continue as crushing capacity appears to have reached its limit.

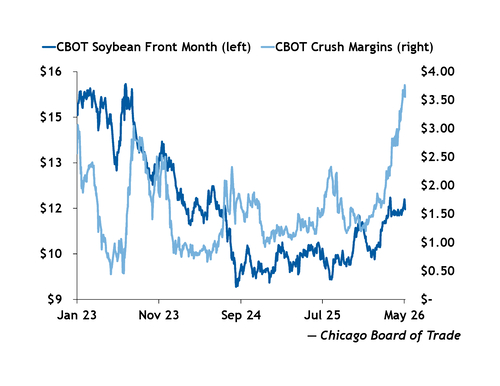

Soybean crush margins on the Chicago Board of Trade (CBOT) — which averaged $1.51/bushel (bu) in 2021-25 — surged to $3.76/bu on 5 May from $2.11/bu on 27 February, supported by rising soybean oil values, which have gained 23pc since the start of the Middle East war. Gains in soybean oil and meal prices outstripped those recorded on soybean futures, in turn widening the CBOT soybean crush margin.

This disconnect suggests US crushers have reached their soybean demand limit. US soybean crushing set a record in March, reaching 92pc of capacity, according to Argus estimates, leaving little room to increase soybean use despite attractive margins.

As a result, US soybean oil and meal outputs may have reached a near-term ceiling. The limited spare crushing capacity would also cap soybean crushing demand, dampening the pass-through of crusher margins to soybean prices.

For margins to revert to normal levels soon, soybean meal and oil prices would need to fall on weaker demand or soybean prices would have to rise on stronger exports — scenarios which face obstacles.

Soybean oil demand hits a new level

Higher energy costs stemming from the war and updates to US biofuels policies have supported — and will likely continue to bolster — US soybean oil prices.

Even if the conflict were to end today, repairing Mideast Gulf infrastructure and restoring trade flows to pre-war levels would take time. And US demand for soybean oil is expected to rise as biofuel producers meet higher blending mandates for 2026 and 2027, with additional support from the 45Z tax credit, which is limited to North American feedstocks.

US soybean oil consumption reached a record 1.22mn t in March, 658,000t of which went to the biofuels sector, up by 74pc on the year, according to Argus estimates. This was the first time since August 2024 that biofuel use accounted for more than half of total soybean oil demand. This share is likely to grow as export demand has already shifted away from the US market.

To meet proposed renewable volume obligation (RVO) targets for 2026, an average of 685,000t of soybean oil per month would need to go to the biofuels sector for the rest of 2026, Argus estimates show. Domestic non-biofuel use has been mostly steady at 546,000t/month since early 2026. But with US soybean oil output capped sy around 1.2mn t/month, supplying both markets leaves little room for additional demand.

Soybean meal in demand, at home and abroad

Strong demand is also supporting US soybean meal prices despite record output from higher soybean crushing.

Total soybean meal use — combining exports and domestic consumption — has held at record levels and exceeded production in five of the first six months of the 2025-26 marketing year, which began on 1 October.

The strength of US soybean meal export demand has come from multiple buyers, with sales to most trade partners up by 10pc or more on the year.

Domestic use has also reached record levels, supported by expanding US poultry and pork production. Domestic consumption through March of the 2025-26 marketing year was up by 1.57mn t from a year earlier. As a result, stocks have stayed mostly below last year, providing support for prices.

With soybean harvests in Brazil forecast to reach record levels this year, export demand could weaken, thereby pressuring prices.

Limited upside for soybeans

A rise in soybean prices, which could narrow crush margins, seems unlikely given the crop's current fundamentals.

Strong crush boosted domestic soybean use by 3.33mn t through March of the 2025-26 marketing year from a year prior. US crushing facilities can process at most 71mn t a year — given daily capacity of 217,000t and allowing for maintenance closures — up about 5mn t from 2024-25.

And export demand for US soybeans has declined following last year's US-China trade dispute. Export sales fell by 8.7mn t through April of 2025-26 from a year earlier, the lowest level for that point in the year since 2013.

As a result, May began with 38.8mn t of soybeans in storage across the US, up by 3.5mn t on the year, according to Argus estimates.

Should farmers plant more soybeans this year to avoid the higher nitrogen fertilizer costs tied to corn production, a large US soybean harvest would carry the domestic surplus into 2026-27. The US Department of Agriculture projected on 31 March that US farmers will plant 3.5mn acres more soybeans than in 2025, based on surveys conducted before fertilizer prices rose due to the war.

The agency will update its acreage projection on 30 June. If farmers have shifted even more acreage into soybeans, prospects for soybean price support will dim further — and the outlook for strong crusher margins will strengthen.

| US soy products supply and use | mn t | ||

| MYTD* | MYTD* Change from prior year | MYTD* % Change | |

| Soybeans | |||

| Crushed | 42.49 | 3.33 | 8.5% |

| Exported | 30.61 | -11.32 | -27.0% |

| Soybean meal | |||

| Produced | 27.30 | 2.10 | 8.3% |

| Domestic use | 18.61 | 1.57 | 9.2% |

| Exported | 9.04 | 0.72 | 8.6% |

| Soybean oil | |||

| Crude oil produced | 7.11 | 0.37 | 5.5% |

| Domestic use | 6.50 | 0.61 | 10.3% |

| -Biofuel use | 2.85 | 0.28 | 11.0% |

| -non-Biofule use | 3.65 | 0.33 | 9.8% |

| Exported | 0.36 | -0.41 | -53.3% |

| * Through March of MY beginning Sep for soybeans, Oct for meal and oil | |||

| — Argus Media, USDA | |||