Maintenance work on the Turkish Stream pipeline has curtailed gas deliveries to central and southeast Europe so far this month, reducing the pace of storage injections and supporting regional gas prices.

Limited arbitrage opportunities have prevented firms from making up for slower inflows on that route through stronger imports from elsewhere, leaving storage as the most economical source of market balancing.

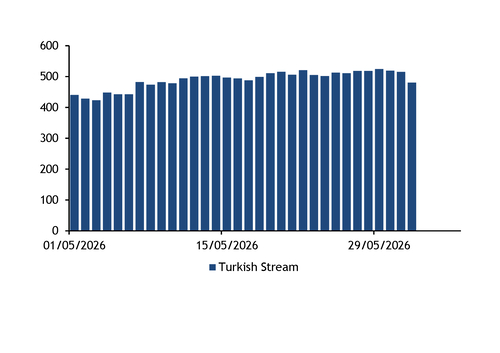

Annual Turkish Stream maintenance is taking place on 2–7 June, with the daily transit nomination at the Strandzha 2 entry point to Bulgaria falling to zero on 2–6 June, the most recent data show. Daily transit deliveries at the Strandzha 2 entry point to Bulgaria were at around 480 GWh/d on 1 June, below around 490 GWh/d in May (see Turkish Stream flows graph). Gas shipped through Turkish Stream supplies Hungary, Slovakia, Serbia and other central eastern Europe markets.

Assuming Turkish Stream remains fully off line until 7 June, countries in central and southeast Europe are set to lose a combined 2.94TWh of supply over the period. But flows on the Turkish Stream resumed one day ahead of schedule last year, at roughly half the rate seen prior to maintenance works.

The loss of flows was largely offset by a slowdown in storage injection rates across the region. Combined injections in Hungary, Romania and Slovakia declined to 64 GWh/d on 2–4 June from around 132 GWh/d in May, while Bulgaria stopped injections on 2 June after building 14.3 GWh/d a week earlier.

Regional prompt prices have risen during Turkish Stream maintenance, increasing their values relative to markets in western Europe.

The Hungarian prompt day-ahead price held an average premium of €1.98/MWh to the TTF on 1-4 June, widening from €0.745/MWh in May. The Slovakian day-ahead price has held €2.41/MWh above the TTF so far this month, widening from €2.08/MWh in May. Bulgarian day-ahead prices switched to a premium of €3.19/MWh from a discount of €0.35/MWh in May (see price graph).

The limited price uplift did not attract additional west-to-east imports, as arbitrage opportunities were insufficient to cover transportation costs. Flows at Baumgarten, Lanzhot and Mosonmagyarovar increased by 19 GWh/d on 2-4 June from 45 GWh/d in May, but this did not compensate for the loss of deliveries on the Turkish Stream. LNG sendout from Greek, Croatian and Polish terminals did not increase. The combined sendout from these terminals so far in June was 292 GWh/d, lower than the 377GWh recorded in May. Alternative supply in the region may come from Azerbaijan through the 11.16bn m³/yr Trans Adriatic Pipeline and imports from Turkey. But deliveries of Azeri gas have been stable at the Kipoi interconnection point on the Turkish-Greek border and have averaged 346 GWh/d so far this month, down slightly from 347 GWh/d in May. Flows at Strandzha 1 have averaged 18.2 GWh/d so far this month, up from 8.3 GWh/d in May, but this increase is also still not sufficient to compensate for the loss of Gazprom's deliveries to the region.