LPG View of the Markets amid the Iran War – March 2026

Prices soared immediately in response to the US and Israel’s attack on Iran and subsequent effective closure of the strait of Hormuz — the vital corridor linking the Mideast Gulf with the international markets. Some 44.2mn t LPG passed though the bottleneck last year, around 3.7mn t/month or 121,000 t/day and equal to 30pc of global seaborne exports. While India and China take the majority of this product — 20.7mn t and 16.2mn t respectively in 2025 — the truly global nature of the market ensured that no regional market has been left unaffected.

Regional summaries

Asia-Pacific and Middle East

The propane Argus Far East Index (AFEI) surged by 53pc over 27 February-18 March following the curtailment of exports from the Middle East. The loss of prompt supply to India and southeast Asia sent these markets scrambling for US supply to bridge the shortfall. Amid intense competition, spot premiums versus April AFEI swaps for 23,000t propane cargoes arriving delivered Japan in April soared to $135/t, up from $55/t.

The butane AFEI increased by 66pc over the same period as lower availability of the heavier grade was met with by outsized demand from south and southeast Asia where consumption is predominantly butane-heavy.

Exports via the strait of Hormuz accounted for 90pc of India’s 23.4mn t of imports in 2025, Kpler data show. New Delhi directed domestic refiners to raise LPG output by about 25pc where the entire domestic production is directed towards household consumers. Offers for April imports were reported at $1,000/t, or $300-400/t premiums to April CP swaps.

Regional ethylene makers maximised switching to LPG amid a shortage of naphtha primarily supplied by the Middle East. Taiwan’s Formosa Plastic procured 46,00t propane for second-half April delivery to Mailiao at premiums to April naphtha quote as LPG proved the cheaper feedstock. But buy tenders for butane were not awarded owing to a lack of offers.

The broadening conflict continues to prolong supply disruption and has propelled propane prices to 12‑year highs, yet Lotte Chemical has issued a tender seeking 46,000t of flexible‑ratio LPG for monthly delivery to Merak, Indonesia over January to December 2027.

Europe

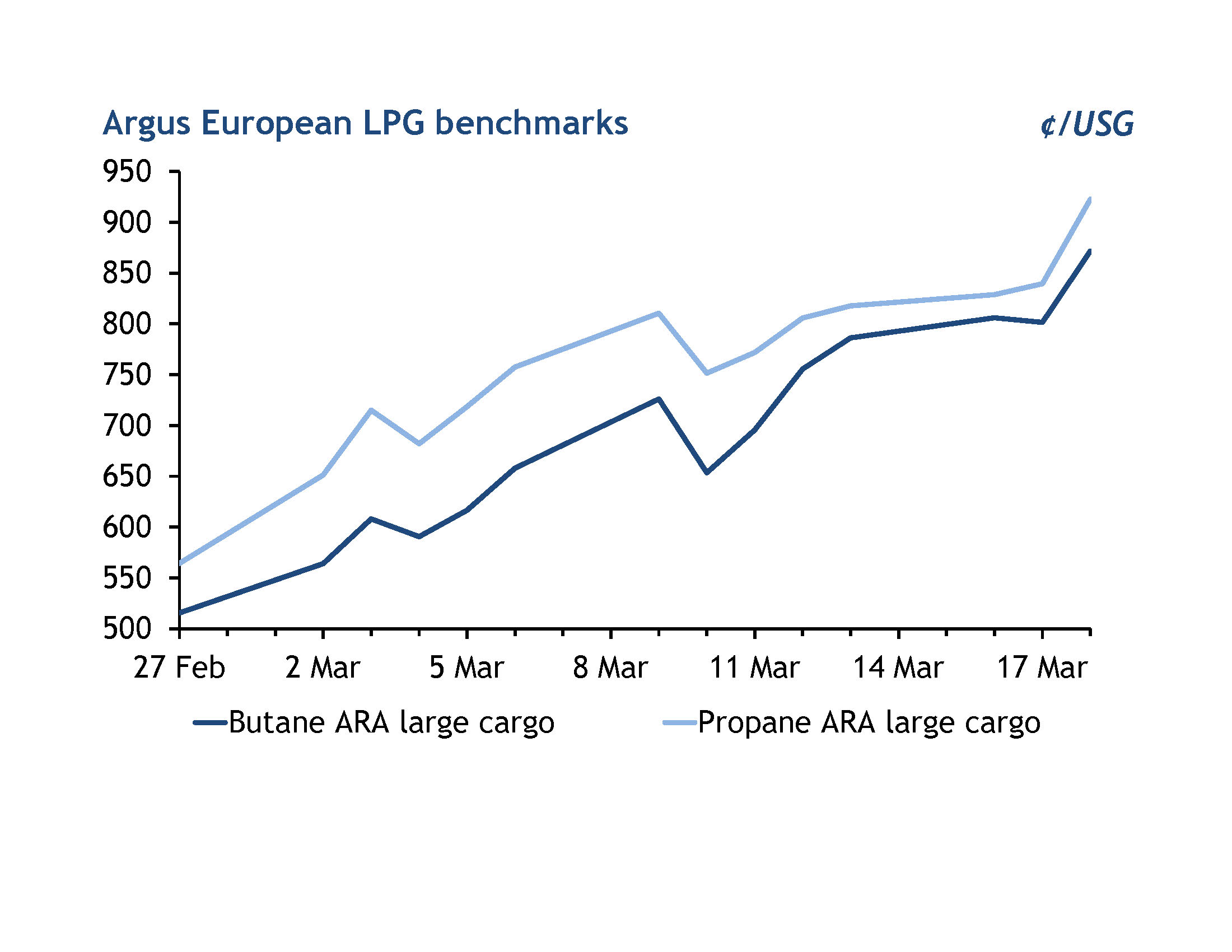

The cif Amsterdam-Rotterdam-Antwerp (ARA) large cargo propane benchmark in northwest Europe rose by 64pc to $922.75/t between 27 February and 18 March, as the conflict in the Middle East triggered a broad rally across the energy complex. Gains outpaced those of crude, with the ratio to Ice Brent futures widening by just over six percentage points to 68.5pc on a dollar per barrel basis, peaking at a three-year high of 69pc on 3 March. Reduced Middle Eastern supply, caused by the near shutdown of the strait of Hormuz, pushed Asian buyers towards US barrels, tightening availability for European importers. Incremental supply from the US Gulf was further curtailed by the force majeure declared at US midstream company Targa Resources’ 472,000 b/d terminal on 18 March.

Large cargo butane prices cif ARA increased by 69pc to $871.75/t over the same period, while the ratio to naphtha firmed by eight points to 96.5pc of front-month naphtha. Persistent strong demand from the Asia-Pacific region continued to draw US volumes eastward, limiting flows into northwest Europe.

Propane railcar premiums to large cargoes eased by 17pc to $104.25/t, as ARA terminals struggled to pass through the full extent of the import price rise to downstream heating markets. Inland buyers retreated in response to higher offers, taking advantage of seasonally lower heating demand, the arrival of delayed February shipments, and a light spring refinery maintenance season.

Supply constraints at regional refineries and prolonged gasoline blending demand lifted the value of butane barges by over 10 points to a four-year high of 116pc cif ARA in the first week of the conflict. The Iran-driven surge in natural gas prices tightened supply further by encouraging refineries to burn butane internally as a fuel. Simultaneously, the loss of supplies through the strait of Hormuz pushed Asia-Pacific buyers to bid for European gasoline, extending the seasonal blending boost.

Argus International LPG is home to global price benchmarks including Argus Far East Index® (AFEI®) and Argus cif ARA large cargoes. Learn more.

Americas

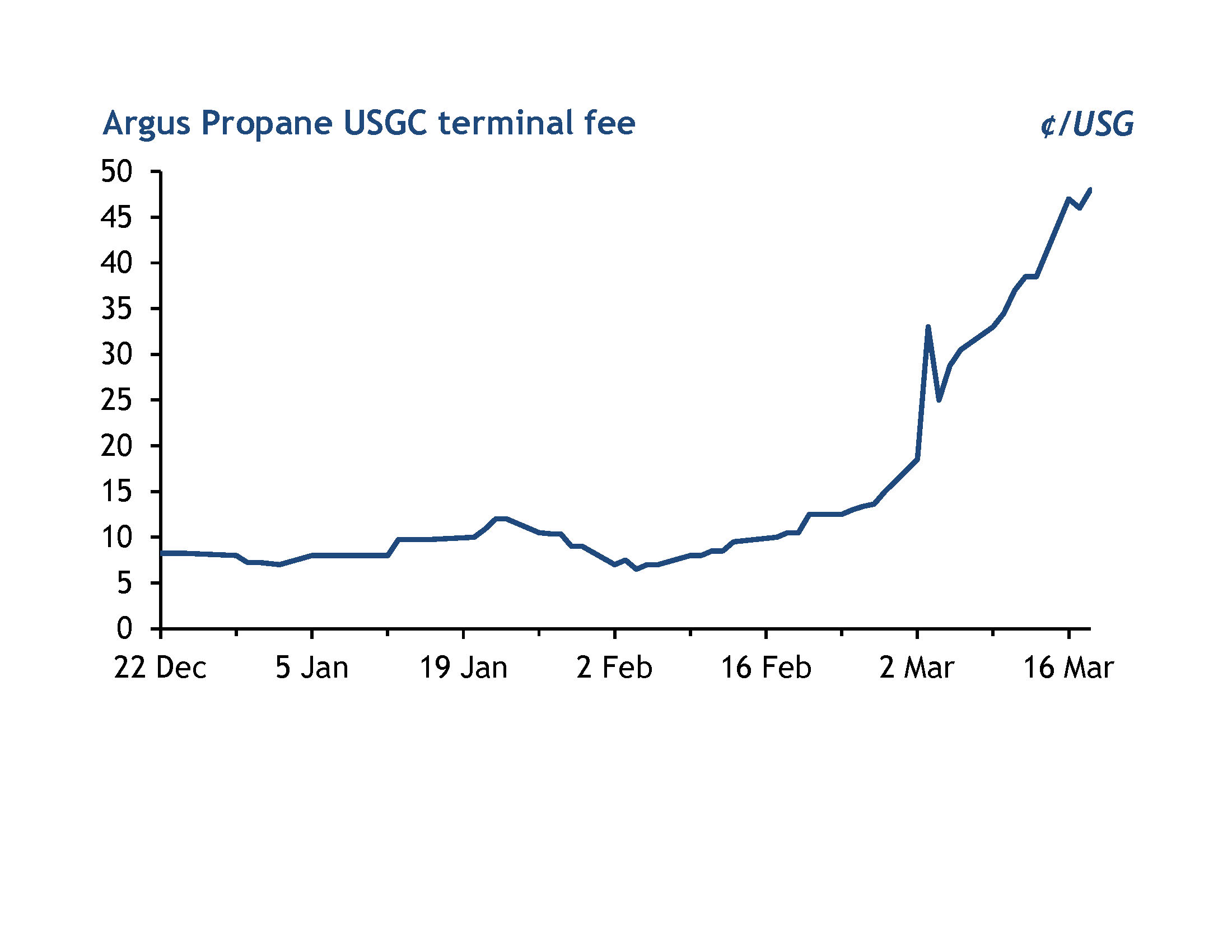

US terminal fees for LPG cargoes surged to more than 10-year highs as tight capacity was met with ever-widening arbitrages to both the US and Asia following the outbreak of the war.

The propane arbitrage to Asia surged to over $500/t on paper on 18 March as attacks on the South Pars field resulted in further curtailments to Mideast production, causing steep gains in Argus Far East Index paper and delivered prices in the region.

Offers for spot-loading propane cargoes out of the US surged to Mont Belvieu EPC +50¢/USG on 18 March, up from the mid-40s¢/USG, after Targa Resources issued a force majeure on loadings out of its 472,000 b/d Galena Park export terminal on the Houston Ship Channel following mechanical problems on its compressors. Targa is now operating at 70pc of its regular capacity owing to the work, according to customers.

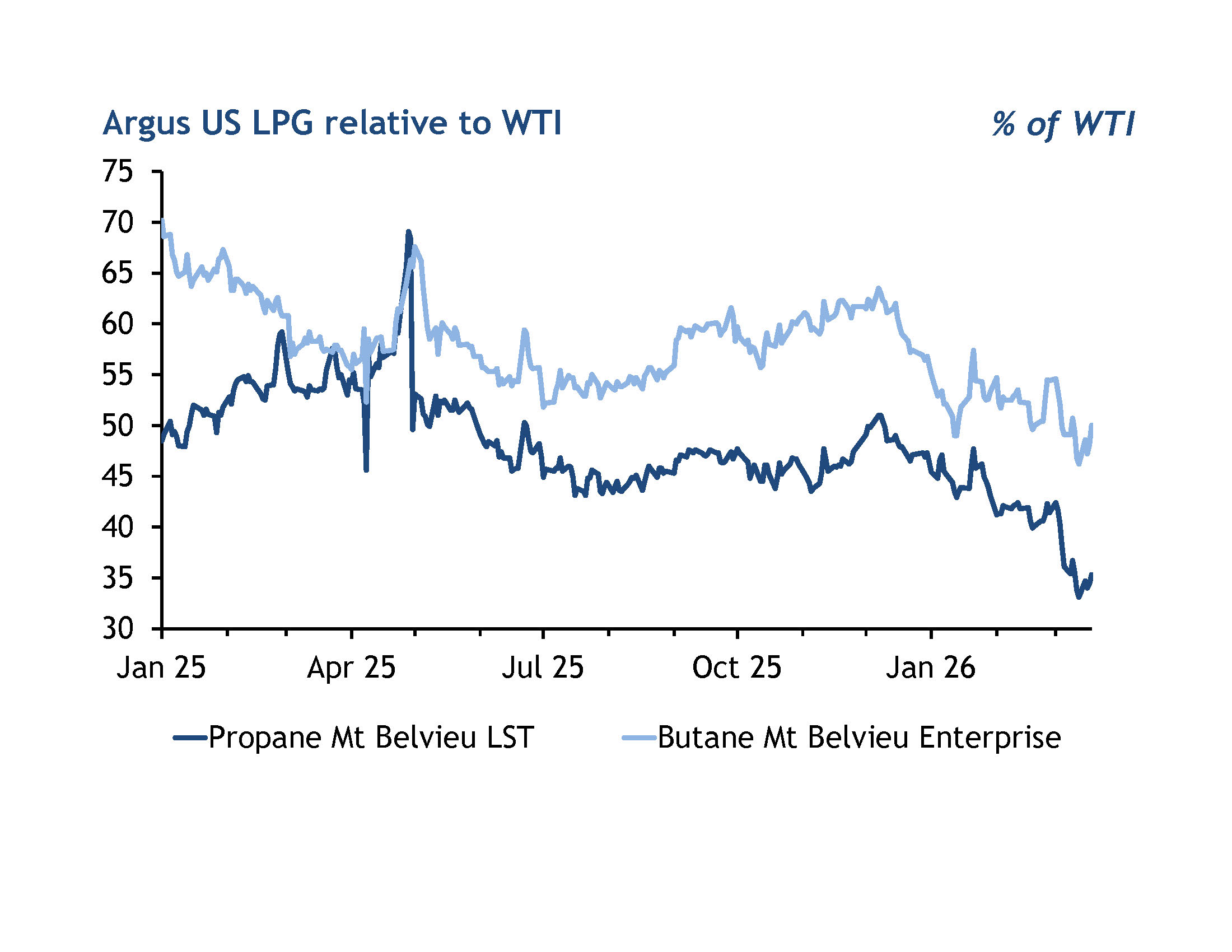

In the domestic US market, propane continued to lag gains in international prices, as US inventories of the heating fuel remain 57pc above the five-year average.

LST in-well prices at Mont Belvieu, Texas, hit an eight-month high of 79.875¢/USG ($416.15/t) 9 March as Nymex WTI topped $100/bl in intraday trading, but have averaged only 37pc of WTI since the war began, well below the 54.4pc during the same period last year.

In-well butane prices at Mont Belvieu surged to 110.75¢/USG ($501.70/t) on 9 March, a more than one-year high, as export demand for split loadings to replace Middle East volumes increased.

Argus NGL Americas delivers trusted NGL price assessments and the latest news for physical markets in North America daily. Learn more.

LPG Market Outlook

The Middle East supplies 3.5mn-4mn t/month of net LPG exports to global markets. The closure of the strait of Hormuz puts the market into a deep deficit, comparable with peak winter heating season, after we expected a balanced market in March before the war.

However inventories are at their seasonal low point, leaving few stocks left to draw to cover the deficit. In addition, the largest stores are in the US, and exports are bottlenecked by terminal capacity, leaving most of world severely short of LPG.

In the short term this deficit will be mostly covered by the petrochemical demand loss and a drawdown of inventories. But very soon demand destruction in residential markets will be needed as shortages persist.

Supplies will remain tight for an extended period, even if the strait reopens tomorrow. Oil and gas fields being shut in will take time to restart, while key infrastructure, such as Ras Laffan and the South Pars facilities, have been damaged and might not be fully operational for several years.

VLGC freight rates have risen in the short term due to disruptions, but we expect the market to normalise and probably turn bearish in April as tonne mile demand falls due to lower global export volumes.

This insight comes from Argus LPG Outlook, a monthly forecast for prices and fundamentals, with expert analysis. Learn more.