Higher demand for downstream products in China and tighter supply during environmental inspections have lifted prices for titanium feedstocks, increasing imports into the country to meet consumption.

The Chinese market for medium-grade titanium ore has turned higher since the start of the month from a near three-year low, on a rise in feedstock costs and renewed buying interest from the titanium dioxide sector.

Spot prices for 46pc grade titanium concentrate were assessed at 1,130-1,150 yuan/t ($159-162/t) yesterday, up from the previous assessment of Yn1,100-1,120/t on 5 September and Yn1,080-1,110/t on 29 August, which was its lowest since November 2016.

The titanium dioxide market moved up last week in response to low inventories and rising offer prices from producers. China-based Lomon Billions, one of the world's largest producers of titanium dioxide pigments, lifted its offer prices on 3 September.

Spot prices for 93pc rutile-grade titanium dioxide increased to Yn14,000-16,200/t on 5 September, their highest since late June, from Yn14,000-15,200/t on 3 September. Export prices rose by $50/t to $2,150-2,250/t fob China, on a rise in buying interest from international consumers because of weakness in the value of the yuan against the dollar.

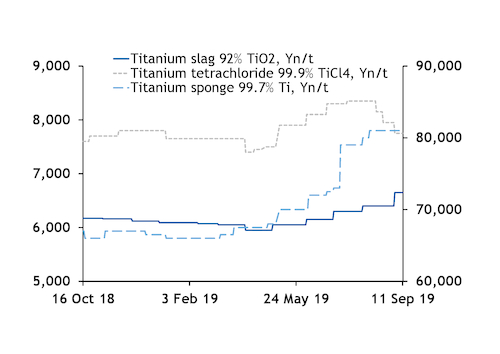

On the titanium sponge market, prices for 99.7pc grade metal have stabilised for the past month at Yn80,000-82,000/t, the highest range since April 2012. Higher costs for feedstock including titanium tetrachloride (TiCl4), tight spot availability and increased demand from titanium mill products manufacturers have lifted the market since March. Titanium products are used across the chemicals, aerospace, medical and military industries, and consumption has been rising this year.

The Chinese titanium sponge market is dependent on imports and demand has increased for material predominantly from Kazakhstan and Ukraine. China imported 715t of titanium sponge in July, trade data show, up from 460t in July 2018 and 557t in July 2017. Imports in January-July this year totalled 4,545t, up from 3,179t in the same period last year and 2,334t in January-July 2017.

The increased demand for metal to be delivered to China has fed into higher prices on the European market, with spot prices for TGTv sponge rising to $7.00-7.50/kg in late August, the highest since November 2017 and up from $6.00-6.25/kg at the end of July.

Output restrictions at small and medium-sized titanium sponge producers have limited Chinese production, owing to tight supply of TiCl4. Producing 1t of sponge typically consumes 4.4t of TiCl4 in China, and increasingly frequent environmental inspections targeting pollution reduction are likely to continue to affect TiCl4 production from titanium slag.

At the same time, the titanium slag market has climbed to its highest level since June 2017 — despite the recent low in concentrate feedstock prices. Inventories have run down as most producers have cut output during the environmental inspections. Spot prices for 92pc grade slag moved up last week to Yn6,500-6,800/t, from Yn6,250-6,550/t previously. The tightening in spot supply of slag has coincided with an increase in demand from the titanium tetrachloride sector.

Chinese titanium producer Jinzhou Titanium Industry has raised its procurement tender price for 90pc grade titanium slag for September delivery to Yn6,350/t delivered and paid by acceptance bill for 5,000t of material, up from Yn6,100/t in its August tender. Jinzhou's titanium slag tender price is used as a reference for spot prices in northern China given the volumes it purchases.

TiCl4 prices reached Yn8,200-8,500/t in mid-August, their highest since November 2012, on higher costs for feedstocks including titanium slag and chlorine gas along with reduced supply from Chinese producer Pangang Titanium Industry during inspections. But the price range has since pulled back to Yn7,500-8,000/t, as prices for chlorine gas have turned lower and demand from the pearlescent pigment and fine chemicals industries has weakened in the past month. Jinzhou Titanium Industry cut its tender price in late August. Most consumers have reduced their bids on expectations of a further fall in prices that could filter up along the supply chain.