Alternative marine fuels

Overview

The marine fuel sector is decarbonising. International Maritime Organization (IMO) requirements and EU legislation is driving this change alongside consumer demand for low carbon solutions.

These drivers have prompted shipowners to invest in alternative marine fuels including; marine biodiesel, bio-methanol, grey methanol, LNG, ammonia and hydrogen.

Argus provides pricing, insights, and intelligence for the fast-growing alternative marine fuels market with independent news, analysis, and market commentary on emerging changes and trends so you can stay ahead.

Argus Market Highlights: Marine Fuels

Get the latest industry news, insight and analysis sent directly to your inbox.

Sign upSpotlight content

Browse the latest thought leadership produced by our global team of experts.

Swiss WinGD sells first ethanol -fuelled marine engines

Swiss WinGD sells first ethanol -fuelled marine engines

Sao Paulo, 19 May (Argus) — Swiss marine engine manufacturer Winterthur Gas and Diesel (WinGD) has sold its first two ethanol-fuelled marine engines. It said last year that it would begin offering the technology . The engines will power two ore carriers to be built for China's Shandong Shipping to operate under charters for Brazilian mining group Vale. WinGD will build the engines by modifying its methanol-fuelled model, as ethanol and methanol share similar properties and combustion characteristics. "This is a clear signal that the shipboard technology and fuel infrastructure around ethanol as a marine fuel are ready, giving confidence to others considering ethanol as an option for maritime decarbonisation," said WinGD executive director of sales Volkmar Galke. Ethanol has gained traction as a marine fuel because of its potential to comply with greenhouse gas (GHG) emissions regulations. Last week, the IMO Marine Environment Protection Committee (MEPC 84) added Brazil's second-crop corn-based ethanol as a recognised fuel pathway in its life-cycle assessment (LCA) guidelines for marine fuels . Although ethanol is not a drop-in fuel, meaning vessels require retrofitting to run on it, it can absorb surplus production from countries such as Brazil. But FuelEU Maritime and the EU Renewable Energy Directive (RED III) — European regulations considered the world's most advanced for shipping — do not accept biofuels made from food crops, known as first-generation fuels, for emissions reduction because of food security risks. By Natália Coelho Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Rotterdam 1Q bunker sales fall sharply

Rotterdam 1Q bunker sales fall sharply

London, 16 April (Argus) — Demand for conventional marine fuels in Rotterdam fell by 28pc on the year in the first quarter of 2026, after the Netherlands implemented the EU's revised Renewable Energy Directive (RED III) at its ports. The decline also reflects disruption linked to the US-Iran war. Market participants reported a drop in Rotterdam bunker demand even before the war, as some shipowners shifted fuelling to neighbouring ports to avoid price premiums created by the Netherlands' unilateral transposition of RED III marine mandates from 1 January. Sales of very-low sulphur fuel oil (VLSFO) fell most sharply, down by 44pc from a year earlier to about 440,000t in the first quarter. High-sulphur fuel oil (HSFO) volumes dropped by 25pc to about 619,000t, while ultra-low sulphur fuel oil (ULSFO) sales fell by 13pc. Marine gasoil (MGO) and marine diesel oil (MDO) demand declined by 8pc on the year to around 361,000t. Some shipowners instead opted to bunker in neighbouring Antwerp, which forms part of the ARA hub and offers lower conventional bunker prices without requiring route changes. Others prioritised bunkering at Gothenburg in Sweden or ports in Germany, market participants said. Price differentials supported the shift. Between early February and the end of March, MGO dob Rotterdam prices averaged $12.75/t higher than the Antwerp equivalent, while VLSFO dob Rotterdam held an average premium of roughly $14.50/t over the same period. Tighter global supply has added further pressure. The effective closure of the strait of Hormuz sharply reduced bunker availability in Singapore, increasing competition for VLSFO and MGO cargoes that would otherwise be exported to the ARA hub. After the start of the US-Iran war, Rotterdam MGO prices rose by 75pc to an average of about $1,186/t in March, while VLSFO prices climbed by 57pc to an average of $710.50/t. By Gabriel Tassi Lara and Hussein Al-Khalisy Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Rotterdam biomarine sales fall in 1Q

Rotterdam biomarine sales fall in 1Q

London, 16 April (Argus) — Marine biodiesel blend sales fell by 35pc in the first quarter compared with the fourth quarter of last year, but were roughly steady compared with the first quarter of 2025. Participants pointed to lacklustre demand in January and February, with an uptick in March as the US-Iran war led to Dutch B100 flipping to a discount against MGO . But these discounts failed to support significant demand growth , as volatility weighed on marine fuel trading activity and buyers hesitant to make significant changes to their procurement strategy based on an acute price spread. Rotterdam's loss has been Singapore's gain. Data from the Port of Singapore showed roughly a 13pc growth in marine biodiesel blend sales on the quarter to the first quarter of 2026. This demand is attributed to FuelEU Maritime requirements, which came into effect in 2025 and require ships coming in, out of, and operating within EU waters to reduce emissions. Shipowners bunkering marine biodiesel in Singapore for EU-bound voyages can use it for FuelEU Maritime compliance. And compliance generated from bunkering marine biodiesel in Singapore can then be used to achieve compliance on vessels operating European routes, via the pooling mechanism, in which obligated companies can combine their compliance balance with other vessels. Bio-LNG sales firmed by 28pc on the quarter in the first quarter of 2026, generating over-compliance which has sold at a significant premium to cost . This may have also weighed on marine biodiesel blend sales, as bio-LNG volumes bunkered would have generated FuelEU compliance surpluses that can then be sold on to vessels that do not have LNG-capable engines. This would then potentially dampen FuelEU-driven demand from those vessels for marine biodiesel blends, and many shipowners did opt to buy surpluses to meet FuelEU requirements. But this dynamic may soon change because of the US-Iran war, where the FuelEU used cooking oil methyl ester (Ucome)–MGO abatement ex-emissions trading system (ETS) price was negative on 7 April. It has since returned to positive levels, marked at €61.45/tCO2e on 15 April. But this remains significantly below FuelEU compliance surplus levels, with offers seen at €175-210/tCO2e, meaning it is currently cheaper to generate compliance using marine biodiesel blends than to buy surpluses to meet the FuelEU requirements. By Hussein Al-Khalisy Rotterdam bunker sales t Fuel 1Q 2026 4Q 2025 Q1 2025 q-o-q % y-o-y % ULSFO 162,142 219,039 187,031 -26 -13 VLSFO 439,804 745,786 789,218 -41 -44 HSFO 619,010 804,962 829,197 -23 -25 MGO/MDO 360,517 402,781 393,071 -10 -8 Conventional total 1,581,473 2,172,568 2,198,517 -27 -28 Biofuel blends 104,630 161,934 104,037 -35 1 LNG (m3) 267,454 192,433 261,200 39 2 Bio-LNG (m3) 15,260 11,932 na 28 na Biomethanol 996 na 5,490 na -82 Port of Rotterdam Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Multi-fuel most sustainable future for bunkers: Panel

Multi-fuel most sustainable future for bunkers: Panel

Singapore, 16 April (Argus) — Ensuring availability of bunkering options for multiple fuels at key ports is the most viable approach to supporting an energy transition in the shipping industry and the establishment of green shipping corridors between key ports, said participants at the Argus Green Marine Fuels conference in Singapore. The US/Israel-Iran war and the subsequent disruptions to conventional bunker fuel supplies from the Middle East has shown that availability of a wider range of fuels will make shipowners less likely to be caught out by supply disruptions, especially for fossil fuels. The port of Rotterdam is preparing for a multi-fuel future like Singapore, said the port's program manager for sustainable transport Naomi van den Berg. "We see it has having a large part to play in moving towards a sustainable fuels future," she said. But infrastructure at ports must be available to support distribution of alternative fuels such as LNG, methanol and ammonia. Ports in Hong Kong are looking to mainland China for support in supplying alternative fuels, said Amy Chan, deputy secretary for transport and logistics for the Hong Kong Special Administrative Region government. Hong Kong is set to announce a partner for its own shipping green corridor later this year, Chan said. LNG remains by far the fuel of choice, based on order books for vessels . But most shipowners are still opting for dual use or considering triple-use engines to ensure they have the flexibility to refuel at ports that offer the best value fuel. The choice of LNG also means shipowners have the option to switch to bio-LNG. Availability of fuels and pricing remain key concerns, particularly in a challenging market, said Rohit Radhakrishnan, chair of the marine fuels committee in the Singapore Shipping Association. Investment in infrastructure is key to ensuring progress and while there are some existing facilities to support the transition to a multi-fuel future, there are still not sufficient infrastructure to fulfill the shipping industry's needs, said conference participants. By Siew Hua Seah Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Refining Under Strain: Supply Disruptions & Rising Oil Market Risk

Refining Under Strain: Supply Disruptions & Rising Oil Market Risk

2026 Guide to European Renewable Fuels Tickets

2026 Guide to European Renewable Fuels Tickets

Why 2026 will be a year of change for US renewable diesel markets

Why 2026 will be a year of change for US renewable diesel markets

Webinars

Biofuels Waste-Based Feedstocks Market Overview and Outlook

As of mid-2025, the waste-based feedstocks market for biofuels in Europe and Asia is experiencing a mix of stability and pressure, shaped by regional dynamics, policy shifts, and changes in global trade flows.

On demand Webinar - 25/06/12SAF Horizons - Global Market Dynamics, Policy Shifts, and Forecasts

We will hear from our freight experts as SAF policy and demand create global trading opportunities in this market.

On demand Webinar - 25/05/21Zooming into the US feedstock market and futures contracts

North America market updates, including recent regulatory changes like 45Z that are driving these markets

On demand Webinar - 25/05/06A webinar series exploring the shifting dynamics in the oil market

Explore how tariffs could influence global oil demand and reshape production dynamics.

Related documents

Alternative marine fuels key prices

Argus Marine Fuels features a comprehensive range of alternative marine fuels prices (in $/t VLSFO, $/t HSFO, and $/t MGO equivalents and $/mn Btu).

Latest events

Argus Green Marine Fuels Europe Conference

Argus Green Marine Fuels Europe Conference

Argus Biofuels & Feedstocks Asia Conference

Argus Biofuels & Feedstocks Asia Conference

Argus Green Marine Fuels Asia Conference

Argus Green Marine Fuels Asia Conference

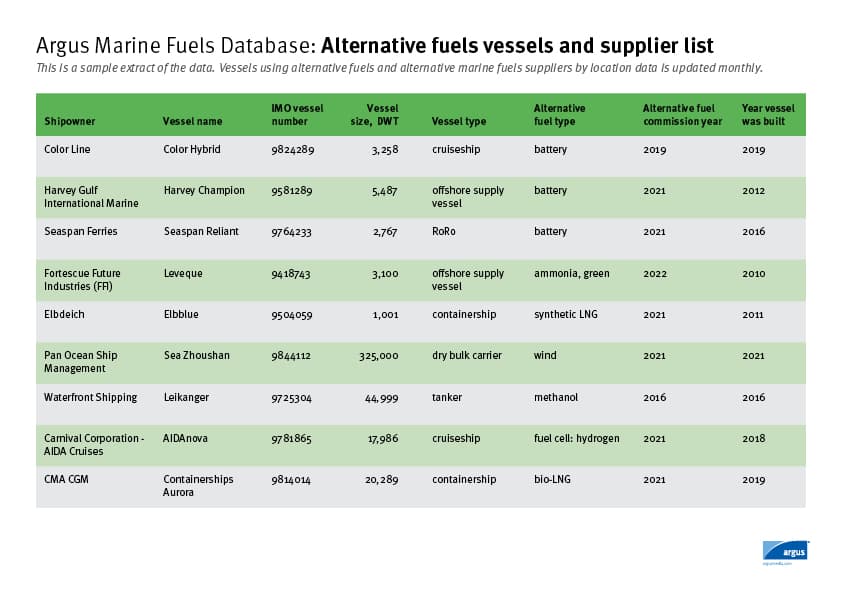

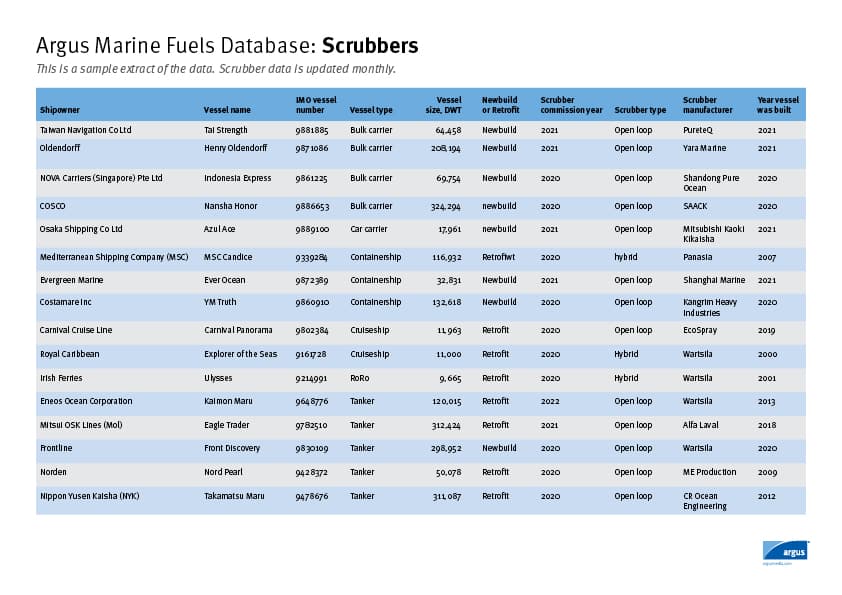

Global alternative fuels vessel databases

Argus Marine Fuels includes access to proprietary data in three downloadable databases, providing essential insights into the changing marine fuels market:

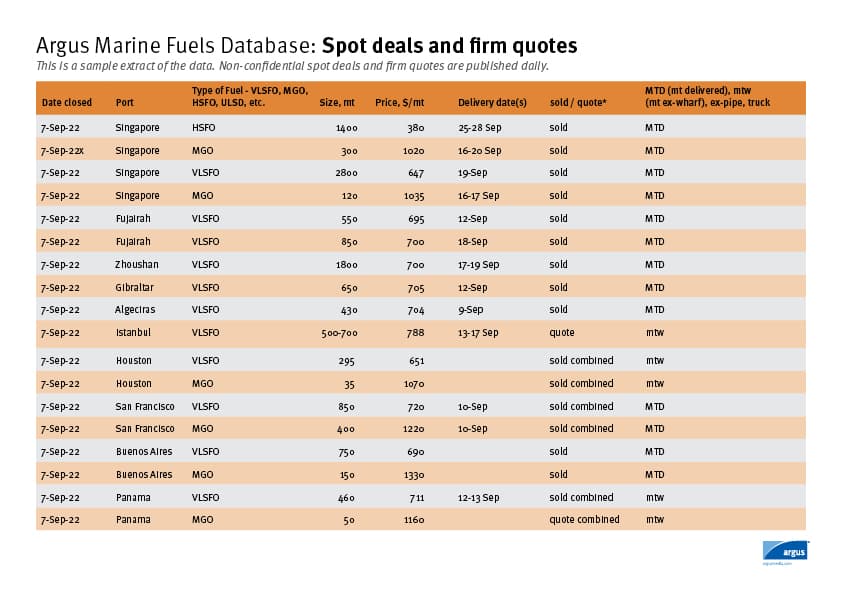

Spot deals and firm quotes

This list of spot deals gives buyers and sellers understanding where they stand price-wise compared with their competitors. Argus’ daily deals/quotes detail the port, type of fuel, size of the deal, price, delivery method and delivery dates. It does not include counterparties’ names.

View sample data

Alternative fuels vessels and supplier list

Argus lists vessels that are burning alternative marine fuels, including methanol, biofuels, ammonia, hydrogen, LNG, LPG, as well as those running on batteries. The database is updated every month.

View sample data

Scrubbers

The database is updated every month. It contains over 4,300 records and counting.

View sample data