Oil and gas producers are increasing their use of near-term hedging to protect revenues in a volatile market, writes Manash Goswami

US upstream independents are adding hedges for the rest of this year and 2020 to mitigate expected oil price volatility, but they are cautious about extending cover beyond this on the possibility that a slowdown in US drilling may strengthen prices.

Many onshore producers seeking to generate stable cash flows and soften the impact of the market downturn are turning to derivatives. These help companies to ensure a minimum price on their oil and gas output, even if market values dip below the floor at which they purchase the contract. But most hedges also come with a ceiling that can limit a producer's earnings in the event that the market strengthens beyond that level, with the gains usually going to the counterparty. And hedging has come under increased focus as investors pressure operators to generate free cash flows and improve margins.

Against this backdrop, Permian basin-focused Pioneer Natural Resources, one of the most well-hedged onshore operators, added further cover for the fourth quarter and initiated hedges for 2020. It now has 110,000 b/d of oil output — half of its production in the third quarter — hedged at $65/bl for the rest of this year. This compares with 72,000 b/d at $67/bl in the second quarter. Pioneer took on derivatives for 2020 for 80,000 b/d at about $63/bl during the third quarter. It will continue to add more for next year, chief executive Scott Sheffield says. But the company will be more cautious for the 2021-25 period. "I am definitely becoming more optimistic that we are probably at the bottom end of the cycle regarding the oil price," Sheffield says.

Bakken operator Whiting Petroleum also grew its hedge book. The company had 67pc of its forecast output hedged for 2019 and 59pc for the first half of 2020, by the end of the third quarter. This compares with 59pc for 2019 and 19pc for January-June 2020 at the end of the previous quarter.

But hedging strategies carry risk in a volatile market. Pioneer made a net derivative gain of $121mn in the third quarter compared with a loss of $135mn a year earlier, and a gain of $150mn in the first nine months compared with a loss of $701mn a year earlier. Smaller peer Parsley gained $57mn on derivatives in July-September, having made a loss of $22.5mn a year earlier. But the firm lost $43.6mn over the first nine months of this year, in line with $42.8mn a year earlier.

Similarly, key Permian operator Concho Resources made a gain of $397mn on derivatives in the third quarter, compared with a loss of $625mn a year earlier. But it still made a loss of $445mn for the first nine months of the year, albeit smaller than the $793mn it lost a year earlier. The company's natural gas hedges helped generate gains in the third quarter, while it lost on oil hedges.

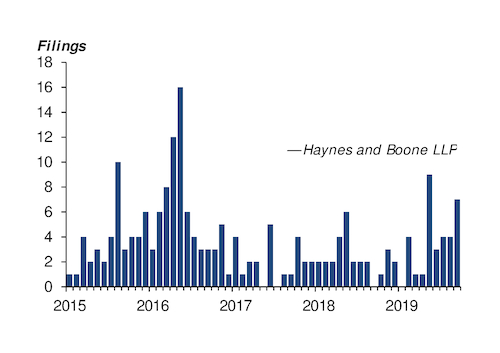

Bankruptcies booming

Financially beleaguered producer Chesapeake Energy has close to 80pc of its oil and gas output in 2019 hedged and continues to add cover for 2020. The firm is seeking to use derivatives to repay debt, which stood at more than 9bn as of 30 September, up from about $7bn at the end of 2018. Chesapeake this month saw off concerns that it might be heading for Chapter 11 bankruptcy protection by securing a new $1.5bn loan facility with a group of banks. But bankruptcies in the North American upstream have been accelerating this year as shale operators struggle to attract financing.

A total of 33 US firms filed for Chapter 11 protection in January-September, with combined debt of nearly $13bn, figures from law firm Haynes and Boone show (see graph). At least three more producers have filed for bankruptcy since then, including EP Energy, an Eagle Ford-focused firm. EP has net debts of $4.6bn, making it the largest upstream bankruptcy filing since SandRidge Energy in 2016.