The US-backed Guaido was sworn in as president of the national assembly this week, but his political footing remains fragile

The White House appears likely to extend a sanctions waiver for Chevron to continue to operate in Venezuela after US-backed opposition leader Juan Guaido overcame a government-backed rival to retain control of the national assembly.

Guaido, accompanied by allied deputies, pushed past heavy security surrounding the assembly on 7 January and was sworn in as the legislature's president for 2020, enabling him to maintain his western-recognised status as Venezuela's interim president. Government-backed deputy Luis Parra and his legislative allies were forced to flee the legislative chamber after the Guaido contingent burst in.

Parra had claimed the previous day to have won an internal legislative election to replace Guaido as assembly president. His disputed election was recognised by Russia, Maduro's main foreign patron. But the US, EU and Canada denounced the Parra vote as fraudulent.

The chaotic developments in Caracas are a setback for President Nicolas Maduro, who has so far withstood US financial and oil sanctions aimed at forcing him out of power in favour of Guaido. The latter declared his interim presidency in January 2019, based on his leadership of the assembly, which is widely seen as the last democratic institution remaining in Venezuela. All other state institutions are controlled by Maduro. But Guaido's political footing remains fragile, amid cracks in the opposition and corruption allegations that he has been accused of doing little to confront.

With Guaido tentatively still in action, the US Treasury appears likely to roll over a sanctions waiver for Chevron as well as a clutch of US oil service companies that expires on 22 January, nearly a year after Washington imposed oil sanctions on the Opec producer.

Opposition officials have indicated support for Chevron to remain in Venezuela, as they see the company as a key future partner for the country's economic recovery under a post-Maduro government. US supporters of a waiver extension argue that Chevron's forced withdrawal would only open the door for deeper Russian and Chinese participation in the oil industry.

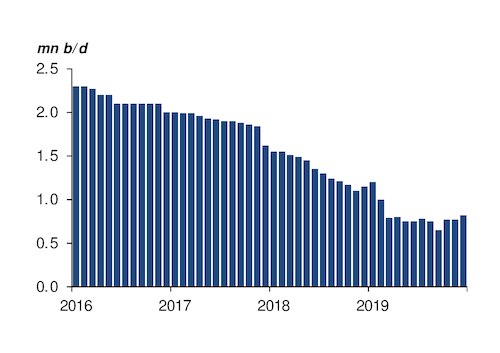

Chevron routinely declines to comment on its Venezuelan operations and the status of its sanctions waiver. The company said in October that it had a "constructive presence" in Venezuela. One of Chevron's key assets in the country is the PetroPiar extra-heavy crude production and upgrading joint venture with state-owned PdV. PetroPiar's upgrader was shifted into less complex blending mode last year, but a tentative industry recovery has enabled the plant to resume upgrading Orinoco extra-heavy crude into Hamaca synthetic crude for export.

Increasingly unrecognisable

While Guaido has managed to maintain his support for now, regional backing for him is gradually eroding. Argentina's new government has withdrawn the diplomatic credentials of his representative in Buenos Aires, Elisa Trotta Gamus.

Argentina was one of several countries in the region — plus the US, the EU and Canada — that recognised Guaido as Venezuela's legitimate president in place of Maduro. But new president Alberto Fernandez has shifted Argentina's stance away from Guaido in favour of a non-interventionist posture espoused by Uruguay and Mexico, two Latin American countries that do not recognise the opposition leader's interim presidency.

Argentina pointedly did not sign on to a new statement by the Lima Group that characterises the Maduro presidency as a "dictatorial regime". The Lima Group comprises Latin American countries plus Canada that co-ordinate peaceful actions to restore democracy in Venezuela.