Somo hopes to turn the country's logistical constraints to its advantage when it comes to Opec's quota negotiations, writes Bachar Halabi

Second-largest Opec producer Iraq's state oil marketing company, Somo, is quietly looking to recast its role in global oil markets, moving beyond its traditional function as a crude seller towards a more strategic posture centred on logistics, optionality and market access. Remarks by Somo director-general Ali Nazar al-Shatari in a recent interview offer a detailed view of how Baghdad is reassessing export routes and infrastructure priorities perhaps also meant to impact its positioning within Opec+ over the coming years.

At a headline level, Iraq's oil narrative continues to revolve around vast reserves, constrained infrastructure and persistent tensions between federal authorities and the Kurdistan region. But beneath that surface, al-Shatari's comments point to a strategy shift focused on controlling how, where and under what conditions Iraqi oil reaches global markets.

Somo estimates Iraq exported around 1.15bn bl of crude last year, generating roughly $84bn in revenue. This compares with exports of slightly more than 1.2bn bl/yr in 2023 and 2024, when higher oil prices pushed up annual revenue closer to $95bn–100bn. Average exports from Iraq's southern terminals stood at around 3.35mn–3.4mn b/d last year, alongside about 200,000 b/d of northbound flows through the Iraq–Turkey pipeline following its partial restart in October.

Somo is explicit that these volumes do not reflect Iraq's underlying production or marketing capacity. "We can market any quantity made available for export," al-Shatari said, arguing that the company's ability to produce exportable crude far exceeds current flows. The binding constraint lies in pipelines, storage and export infrastructure, rather than in demand or sales capability, al-Shatari said.

Framed this way, Baghdad would argue that spare capacity exists, even if it is not immediately deployable. This comes against a backdrop of Iraq having pushed — both privately and openly — for a higher production baseline within the Opec+ alliance. The timing is significant, given Opec+ is conducting its maximum sustainable production capacity assessment this year, with a view to recalibrating quotas by late 2026. But unless those logistical bottlenecks are actively resolved, they will also limit Iraq's ability to argue for a higher production baseline under the MSC assessment.

Revenue reasoning

For Iraq, the debate is not solely about capacity recognition. Oil revenue is central to state finances and political stability, funding an expansive public payroll and a state apparatus heavily reliant on salaries and transfers to public servants. Baghdad is making the case that latent supply growth is structural, anchored in upstream capacity, but constrained by infrastructure rather than policy choice.

Still, Somo's assertion of near-unlimited marketing capacity warrants caution. Iraqi crude remains structurally competitive but global oil demand growth began to slow last year and is expected to moderate further in 2026. In Asia-Pacific, refinery utilisation is increasingly shaped by margins, maintenance cycles and product market conditions, limiting the region's ability to absorb additional crude supply on a sustained basis. European appetite for Iraqi sour crude has strengthened following the loss of Russian supply, but it too is finite.

Freight availability, insurance cover, sanctions compliance and refinery crude compatibility continue to place practical limits on the market's ability to absorb additional Iraqi output. These factors influence which buyers can take more of Iraq's crude and at what cost. In that context, Somo's confidence reflects less an assumption of unlimited demand than a calculation that improved logistics and route flexibility will shape Iraq's effective export capacity.

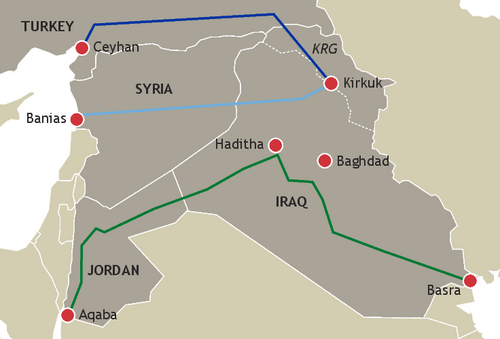

Nowhere is this more evident than in Somo's renewed focus on Turkey's Ceyhan terminal. The Iraq–Turkey pipeline's twin lines have a combined nameplate capacity of about 1.4mn b/d, according to al-Shatari, yet only a fraction is currently utilised. Somo says negotiations with Ankara on a revised framework agreement are progressing positively, with draft texts being exchanged and both sides aiming to reach an agreement later this year.

Somo views Ceyhan as a strategic outlet for Iraqi crude into Europe and the Americas, reducing reliance on southern export infrastructure oriented primarily towards Asian buyers. Operational challenges on the route are ongoing following a spat between Baghdad and Turkey that left the pipeline shut down in March 2023-September 2025, but all parties involved, including Turkey, share an interest in keeping exports flowing. The arrangement's durability will depend on political continuity in Baghdad, co-operation from the Kurdistan Regional Government and Ankara, and a local geopolitical environment prone to sudden shifts.

For Opec+, the deal carries wider significance. By placing northern exports under a single federal marketer, it clarifies Iraq's export volumes and reduces uncertainty over its Opec compliance — long a source of friction within the group.

Al-Shatari outlined the firm's longer-term plans to route Basrah crude northwards and separate storage at Ceyhan to handle multiple grades, increasing flexibility in allocating supplies. The company's push to diversify export routes reflects not only commercial logic but also recent experience. During the 12-day Israel-Iran conflict last June, Iraq confronted the risk of disruption at the strait of Hormuz, highlighting the vulnerability of relying on a single southern outlet.

In contrast, al-Shatari offered a blunt assessment of the long-planned Basrah–Aqaba pipeline project, to ship crude from Iraq to Jordan's Aqaba port. Al-Shatari acknowledged the project's political and crisis-response value but questioned its economic rationale, noting that exports out of Aqaba would still require transit through the Suez Canal or Egypt's Sumed system to reach Europe, while offering limited advantages for Asia-Pacific buyers. Security risks in the Red Sea further weaken the project's appeal, he said. The remarks are a clear departure from former prime minister Mustafa al-Kadhimi's earlier official backing of the line.

The most forward-looking element of Somo's strategy lies in offshore storage. Iraq has signed initial agreements with Oman to develop crude storage at Duqm, with potential for expansion to Ras Markaz and Mina al-Fahl. These Omani ports can accommodate very large and ultra large crude carriers, offering scale and flexibility unavailable at Iraq's southern ports.

Think strait

Storage outside the Mideast Gulf would reduce exposure to weather disruptions and geopolitical risks around the strait of Hormuz, while also placing crude closer to Asia-Pacific buyers. Al-Shatari confirmed Somo is in talks with ExxonMobil on storage and trading options in Asia-Pacific, including Singapore, China and India, such as leasing tanks, profit sharing and possible joint ownership. These steps point to a gradual shift towards greater control over timing, routing and destination.

But despite diversification efforts, Asia-Pacific remains Iraq's main destination and revenue source. While most contracts are annual, some Asian buyers are tied into supply relationships lasting 10-15 years. Pricing is uniform, with priority granted through volumes and loading schedules rather than discounts. This means a large share of Iraqi crude is committed, limiting short-term flexibility.

Taken together, these elements explain how Iraq may navigate its oil policy and Opec+ politics in the years ahead. By stressing logistical limits, Baghdad can argue it holds spare production capacity without lifting crude exports, while expanded routes and storage improve resilience. Whether this flexibility remains dormant or becomes market-moving will depend on Iraq.