ARA biofuels decouple from fossil complex as jet, gasoil prices surge

The surge in fossil fuel prices as a result of the war in the Middle East contrasted with more moderate changes in northwest European biofuels prices over the same period highlights the different fundamentals of fossil and bio markets, and underscores the need for market-reflective pricing to index biocomponents blended into transport fuels.

Geopolitical tensions and chokepoints on key trading routes have disrupted global fossil fuel markets, while biofuels markets still take their lead from domestic renewable fuel policy and contend with their own supply and demand fundamentals.

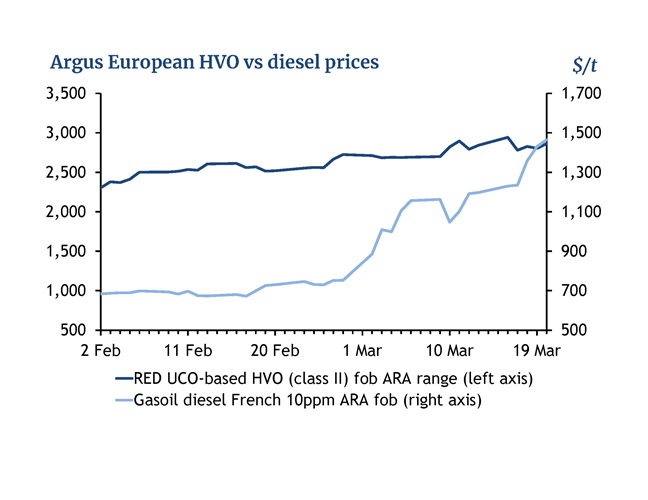

Diesel prices have risen by around 95pc between 27 February and 20 March, and the cost of jet fuel cargoes has more than doubled in the same period, hitting a record $1,795/t on 19 March. Meanwhile, the premium to gasoil for used cooking oil (UCO)-based methyl ester biodiesel dropped by 55pc, while the outright value was only 12pc higher between 27 February and 20 March. And the premium to gasoil for UCO-based hydrotreated vegetable oil (HVO) slipped by around 23pc from pre-war levels by 20 March, while the outright price was 5pc higher compared with 27 February.

Biofuels premiums have been falling in part to offset gains in the fossil complex, but outright prices are still impacted by EU-specific renewables policies. For example, all HVO outright prices fell on 17 March because Germany decided to remove the transposition of the recast EU renewable energy directive (RED III) and the domestic greenhouse gas (GHG) quota from the parliamentary agenda for 19 March, leaving the timeline for implementation unclear and 2026 biofuels demand uncertain. It also expanded the list of feedstocks that it considers "advanced" for HVO production — widening the pool of raw materials that can be used to meet the national obligation. But when gasoil and diesel prices surged in the following days, HVO outright prices were much more stable.

Sustainable aviation fuel (SAF) in the form of hydrotreated esters and fatty acids synthesised paraffinic kerosine (HEFA-SPK) could appear to be an exception to the trend in the European bio-complex, having strengthened by 27pc in the 27 February-20 March period on an outright basis. But a closer look at its differential with the northwest European jet cargo price reveals a similar story. Jet prices have been the most affected across the middle distillates barrel by the conflict, hitting several record highs since 27 February, and increasing by around 116pc above pre-war levels by 20 March.

Around 20pc of global jet fuel flows, and approximately 50pc of all European supply, pass through the strait of Hormuz. Pressure from the aviation complex has had spillover effects in the SAF market, adding to SAF-specific supportive fundamentals.

Supply of HEFA-SPK in Europe appears relatively tight for March and April, owing to slightly stronger spot buying, some plant maintenance, slower imports from Asia, and European producers focusing on making HVO instead. Freight costs have also risen to import new cargoes of HEFA-SPK.

Although both HEFA-SPK SAF and HVO are produced through hydrotreatment of oils and fats, HEFA-SPK requires additional processing and is more expensive to produce. Despite this, a modest 2pc blending mandate, different duty treatment and sufficient supply have meant that HEFA-SPK has often priced at a discount to HVO since the start of the EU and UK SAF mandates in 2025, prompting producers to maximise renewable diesel output where possible.

And despite a 27pc increase in the HEFA-SPK SAF fob ARA range benchmark from 27 February, its premium to jet cargo prices has narrowed by more than $320/t, or around 21pc, since the start of the war.

Author name: Argus Business Development