The Crude Report: WTI swallows Brent

The world’s most important crude oil benchmark (Brent) is now directly tied to the world’s most dynamic crude market (WTI) – there is still an ocean between them, but the reality is that WTI is setting the pace for Brent and everything linked to it. One could argue that Brent is simply WTI in disguise, and that for simplicity’s sake an increasing volume of international oil trade will be linked to indexes generated at the US Gulf Coast, rather than in Europe.

It has finally happened.

The change that the oil market has long been agonising over – the inclusion in the Brent basket of US WTI crude delivered into Europe – took place in May this year.

This is the most radical change to the world’s premier commodity benchmark since its inception, and is intended to remedy the declining physical volumes in the Brent basket of crude oils: Brent, Forties, Oseberg, Ekofisk and Troll.

Production of those crudes has been falling for years, dropping below 1mn b/d for the combined five in 2018, and down to just 713,000 b/d last year. That is only around one cargo a day. And volumes have continue to fade – in August this year only 565,000 b/d is scheduled to load.

By contrast, almost 1.7 million barrels a day of US crude has been making its way to Europe this year, and the vast majority of that has been light sweet WTI Midland crude

This has more or less replaced the barrels lost since Russian crude was diverted away from Europe in 2022, first because of self-sanctioning, and then as the result of a formal embargo in the wake of Russia’s invasion of Ukraine. Russian Urals, once the bedrock of European refining, is now mostly going to India and other points east, leaving Brent without a foundation.

The Urals-shaped hole in the European market meant that the solution to the Brent problem of adding imported WTI crude to the Brent basket – first proposed and demonstrated by Argus in February 2019 – moved from being compelling to being irresistible.

First, Shell updated the terms of the standard forward Brent contract (STASCO BFOETM 2022) to allow for the delivery of WTI Midland to satisfy forward Brent positions from June 2023 onwards, then both leading price reporting agencies, Argus and S&P Global Platts, began to include WTI Midland (delivered Rotterdam with a cross-North Sea freight deduction) in their respective North Sea Dated and Dated Brent assessments from May.

The impact was instant.

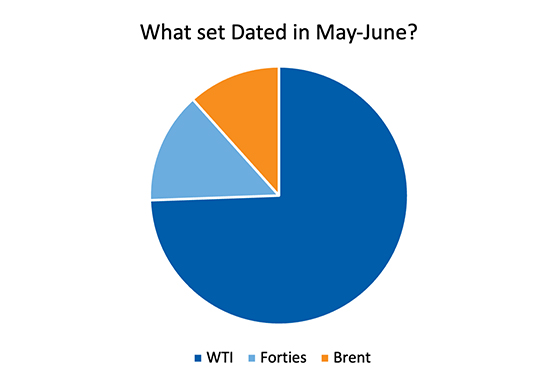

In the month of May, WTI set the benchmark (by being the cheapest of the grades in the basket) on 14 days out of 20, and in June it set the price 18 sessions out of 22. And when we compare the price outcome from the new pool with the old, using Argus’ Dated BFOET (without WTI) for comparison, the benchmark has been on average 16c/bl lower, and at times up to 81c/bl lower, than it would have been without WTI included.

In the Dated market in June, 13 WTI cargoes traded on a delivered Rotterdam basis, compared with just five cargoes of the other five grades combined. And there were 94 bids and offers for delivered WTI in June, against just 35 bids and offers for the other five grades. So the volume of information available to PRAs (Price Reporting Agencies) like Argus in order to determine the benchmark value is some two and half times greater now than before.

Meanwhile, the market for the forward or cash Brent contract ballooned in June, with 19.8 million barrels of this contract traded or 28 full cargoes, more than double last year's monthly average the highest volume for any month since 2016. When participants buy cargoes through this market, in theory any grade of Brent, Forties, Oseberg, Ekofisk, Troll or WTI can be delivered. But in the past two months, it has been almost exclusively WTI that is delivered into this contract.

Buy Brent, get WTI

In short, the Brent complex has become a delivery mechanism for WTI Midland, and the Brent price has become, essentially, the price of WTI delivered to Rotterdam.

The reason WTI is cheaper, despite being higher quality light sweet crude, is partly that it is being traded in a prompter timeframe – allowing it to converge with the 10- days-to-a-month-ahead loading date-range for Brent and its North Sea peers. Also, the fact that no loading or delivery programme for WTI is published ahead of time, unlike for the BFOET grades, means that the amount of WTI that can be delivered into Brent is unknowable. There is no need for any buyer to bid up the price of WTI at Rotterdam, because another cargo can always be found. So the risk to the price of Brent of the pool change is always to the downside.

Brent = WTI Houston + freight to Rotterdam

One of the most keenly watched spread values in oil has long been the WTI-Brent relationship – an easily traded shorthand for the transatlantic crude arbitrage. One of the concerns heard in the market ahead of this year’s change was that the Brent price would simply become the European price for WTI. And if that is the case, how does one measure the transatlantic arbitrage?

The relationship between Brent futures and WTI futures has become closer and more stable. The front month Ice Brent futures contract traded at an average premium to the front month WTI contract in the second half of last year of $6/bl a barrel, and it was the same in the first quarter of this year, but since the start of May when WTI was first added to the basket, that spread has narrowed to just $4.35/bl a barrel and is significantly more stable since the change.

![]()

The spread is easily calculated by taking the Argus assessment of the WTI Houston differential and then adding the freight across the Atlantic. But adding freight to a crude price is not the same as understanding the arbitrage between two different regions. How do we know whether it is better to send crude to Europe or to Asia if the European Brent price and by extension the Asia price are just derivatives of the same WTI fob price?

Essentially the main benchmarks have become two faces of the same coin, or rather, two ends of the same piece of string, where the string represents the freight cost. In recognition of this, the US Gulf Coast crude markets have become more active than ever as a wider pool of participants seek to increase their exposure to the real focus of price discovery.

The Argus WTI Houston price, based on a volume-weighted average of trade, has topped 1mn b/d for the July trade month, by far the biggest ever seen in that market. A lot of that growing activity is the work of international players keen to secure WTI supply in order to bring it to Europe or wherever it is most in demand, as well as to link the pricing of WTI cargoes to the most liquid and appropriate instrument. Already some refiners in Europe and elsewhere are purchasing WTI Midland for loading at the US Gulf Coast on an Argus WTI Houston basis, rather than waiting for Brent-related delivered offers. There has also been a huge surge this year in the use of the derivatives that settle against those Argus WTI Midland and WTI Houston differentials – making them, when combined, the third largest crude futures contracts, after Ice Brent futures and Nymex WTI.

Liquidity begets liquidity, and it may be that we are seeing the beginning of a shift in crude pricing practice. For the time being, Brent remains deeply embedded in the global commodity trade – too big to fail. But the Dated Brent complex remains fiendishly complicated. As the market comes to realise that today’s Brent is simply WTI in disguise, it may be that for simplicity’s sake an ever-increasing volume of international oil trade will be linked to indexes generated at the US Gulf Coast, rather than in Europe.

Author Michael Carolan, Lina Bulyk and James Gooder