PVDF demand to increase chlor-alkali consumption

PVDF demand to increase chlor-alkali consumption

The demand growth of polyvinylidene fluoride (PVDF) is dependent on lithium-ion batteries for battery-operated electric vehicle (EV) demand and stationery electrical storage. Argus forecasts global lithium-ion battery demand in EVs to reach 3.8GWh by 2034 from 0.7GWh in 2023. EV sales are expected to rise at an average growth rate of 10pc in the next 10 years reaching more than 46mn units.

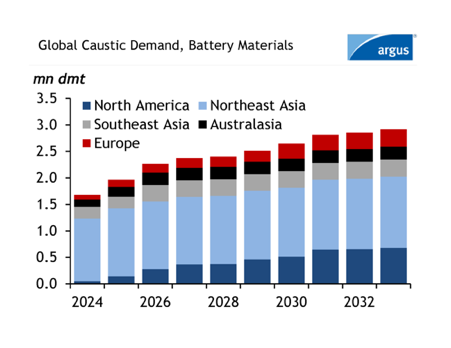

Global caustic soda demand into battery materials for leading regions is shown in the figure. Argus’s latest caustic soda analytics forecast explains an exponential rise in caustic soda consumption for battery material processing. Global caustic soda consumption in the processing of lithium hydroxide, lithium carbonate, cathode materials and recycled black mass was at 1.5mn dmt in 2023 and is expected to reach 3mn dmt in 2033 at a CAGR of 10pc in the first five years.

The relationship between chlor-alkali products and battery materials is gaining focus in the market. With increasing Lithium-based battery capacity globally, demand for associated battery materials is expected to rise. Among the other components of the Li-ion battery stack, PVDF plays an important role as a binder and separator coating, optimizing energy storage efficiency and reducing battery weight in EVs.

PVDF utilizes caustic soda and chlorine in its production at different stages. Primary feedstock includes vinylidene chloride or vinylidene fluoride, which are derivatives of caustic soda and chlorine.

Some significant developments in PVDF capacity are taking place in North America and Northeast Asia. Belgian chemical company Solvay entered into a joint venture with Mexico-based PVC producer Orbia to build the largest production facility of battery-grade suspension PVDF in North America with a capacity of 20,000 t/yr. Commercial production is expected to start in 2026 and the expected caustic soda and chlorine demand can be 8,000 t/yr and 12,000 t/yr respectively.

Solvay has doubled its capacity in Changshu, China in the past five years and raised its capacity in France by 35pc reaching 35,000 t/yr making it the largest production site in Europe. Another major producer French chemical company Arkema increased production capacity by 50pc last year at its Changshu site in China.

Japan-based producer Kureha is undergoing expansion at its Iwaki site in Japan, having a production capacity of 6,500 t/yr. The expansion is in two phases, first is a new capacity of 8,000 t/yr and another 2,000 t/yr in the second phase by debottlenecking resulting in a total capacity of 20,000 t/yr by 2026.

This article was created using data and insight from Argus Caustic Soda Analytics and Argus Battery Materials.

Spotlight content

Related news

Ceasefire offers little relief to Indian plastic makers

Ceasefire offers little relief to Indian plastic makers

Mumbai, 9 April (Argus) — The fragile ceasefire between the US and Iran is unlikely to offer an immediate respite to Indian plastic converters who are grappling with rising feedstock prices that are eroding their production margins. Since the Iran war began, prices have increased by nearly 50pc, with no indication that they will decrease anytime soon. Indian PP raffia prices were last assessed at $1,300-1,400/t cfr India on 2 April, up by $445/t or 49pc compared with $890-920/t on February 27 before the war started. Indian low-density polyethylene prices were assessed at $1,600-1,700/t cfr India on 2 April, up by $580/t or 54pc compared with $1,060-1,080/t on February 27. Lower polymer imports from the Middle East and rising domestic prices are putting pressure on plastic converters which manufacture packaging materials among other products. And their customers, such as fast-moving consumer goods (FMCG) firms, are reluctant to accept the hike in packaging material costs, leaving them in a challenging situation. "A large percentage of plastic converters in India are micro, small and medium enterprises, who have been hit the worst," Amit Kumar Agarwal, the President of Indian Plastics Federation (IPF), told Argus . Even for orders that were booked before the war, suppliers are demanding surcharges amounting to hundreds of dollars per metric ton due to shipping constraints, which are adding more pressure on converters. Middle East imports hit The Middle East conflict has put at least of half of India's total polymer imports in jeopardy, as the Gulf Co-operation Council (GCC) countries supply most of the imports. For 2025, the Middle East supplied around 62pc of India's polyethylene (PE) imports, or 1.41 mn t. The region also supplied 51pc of India's polypropylene (PP) imports, or 930,000 t. The de facto closure of the strait of Hormuz has led suppliers to use Oman's East Coast ports such as Salalah and Sohar to send limited material. But overall exports from the region remain significantly reduced since the war. The market is also sceptical about whether the ceasefire will hold and for how long. Less than 24 hours after the announcement on Tuesday, the two sides are offering conflicting accounts of key terms of the ceasefire and of a potential peace agreement. Attacks on energy infrastructure in Iran and in neighbouring Mideast Gulf states continued in the hours after the ceasefire was announced. Even if the conflict ends, there's no certainty on product availability as several petrochemicals production units have been hit in missile and drone attacks, Dubai-based traders said. Petrochemical producers in the Middle East, including UAE's Borouge and Kuwait's Petrochemical Industries Company, faced drone and missile attacks on Sunday. Iranian attacks also caused fires in Saudi Arabia's Jubail — a key hub for petrochemicals. Supply crunch goes on In India, domestic producers have had to cut production further tightening supply. State-controlled Indian Oil, Mangalore Refinery and Petrochemicals (MRPL), HPCL-Mittal Energy, and Reliance Industries (RIL) have all cut PP output , after the Indian government asked refiners to divert propane, butene and propylene toward cooking gas production, limiting feedstock availability for petrochemicals. "We have only passed down the higher feedstock costs partially," an official with a state-owned producer said. Several producers expect prices to stay elevated in the near-term unless the feedstock prices come down. State-owned Opal and Gail also cut production, squeezing PE supplies. To alleviate the pain of high feedstock prices, the Indian government slashed import duties on petrochemicals products to zero until the end of June. But this has had little effect on offers from China, which has stepped in to fill the void left by Middle East producers, several traders said. Following the ceasefire announcement on 9 April, some China-based traders cut their offers. But others continue to offer at high levels citing market uncertainty and high Indian domestic prices. The IPF has written to the government to extend the import tax waiver for six months as the war could go on for a long time, Agarwal told Argus . The outcome of that petition is awaited. Sooner or later consumer product makers will need to pass the higher costs to the end-users. The Indian consumers will likely feel the impact of rising packaging material costs from this month with producers either hiking prices or cutting volumes, Dhairyashil Patil, president of the All India Consumer Products Distributors Federation, told Argus . By Sourasis Bose Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

EIA raises US NGL production, demand forecasts

EIA raises US NGL production, demand forecasts

Houston, 8 April (Argus) — The US Energy Information Administration (EIA) raised its 10-year outlook for average production of natural gas plant liquids (NGLs) by 14.4pc. In its Annual Energy Outlook (AEO), the EIA estimated production of NGLs would average 8.85mn b/d from 2026 to 2035, up from the estimate of 7.74mn b/d for that period in its report last year . By 2050, production will reach 11.3mn b/d, EIA said, a 32.3pc hike from the agency's previous 2050 forecast. Consumption of hydrocarbon gas liquids (HGLs), which the EIA defines as ethane, propane, normal butane, isobutane, natural gasoline, and refinery olefins, is projected to average 3.82mn b/d over the next 10 years, up from the 3.69mn b/d forecast in the 2025 AEO. The agency continues to expect much of this demand to come from the industrial sector, including petrochemical manufacturing. EIA forecast 3,710 trillion Btu/y of industrial-sector HGL consumption between 2026-2035, up from its 3,630 trillion Btu/y forecast for the period last year. EIA also raised its estimate for domestic propane use in the residential, commercial, and transportation sectors across the period to 727 trillion Btu/y, up from 697 trillion Btu/y as estimated in 2025. The increase was almost entirely attributable to the residential sector, which the agency predicts will consume 485 trillion Btu/y, up from its previous 456 trillion Btu/y forecast for the period. By Joseph Barbour Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Brazil's Braskem on brink of control reset

Brazil's Braskem on brink of control reset

Sao Paulo, 8 April (Argus) — Brazilian petrochemical producer Braskem secured the EU's competition clearance on 8 April, the last regulatory obstacle to its long-anticipated change of control. The transition is no longer a matter of approvals but of execution, placing governance mechanics, creditor coordination and shareholder alignment at the center of the company's near-term agenda. The transaction will introduce a new joint control structure, transferring voting power away from its former controlling shareholder, fellow conglomerate Novonor, through a debt-backed equity conversion while preserving a significant strategic role for state-controlled oil firm Petrobras. The framework has now been accepted across the jurisdictions most relevant to Braskem's industrial footprint — Brazil, the US, Mexico and the EU — leaving the completion of documentation, share transfers and the activation of a revised shareholders agreement as the remaining steps before the new structure becomes effective. The EU nod follows Brazil's antitrust authority Cade approving without restrictions on 6 March and the transfer of Novonor's stake in Braskem to an investment fund advised by IG4 Sol, marking a significant shift in the long-running dispute over control of the petrochemical producer. IG4 Sol is part of IG4 Capital, a private equity firm specializing in distressed assets. Its proposal involves acquiring Novonor's debt from a consortium of banks — including Itau, Bradesco, Santander, Banco do Brasil and national development bank Bndes — and converting it into equity in Braskem. This debt-for-equity approach could allow IG4 to assume Braskem's control without a direct share purchase. These steps carry meaningful implications for Braskem's operational latitude. Prolonged uncertainty over control has limited the company's ability to take decisive action on capital structure, portfolio optimization and longer term investment planning. Finalizing the control transition would remove a key overhang that has constrained strategic decision making during a prolonged and punishing petrochemical downturn. Timing The timing of the control reset is delicate but potentially consequential, as Braskem begins the second quarter after an extended period of margin compression driven by global oversupply, subdued demand and elevated fixed costs. Company disclosures have consistently highlighted pressure on cash generation and leverage, even as liquidity buffers have remained intact. Against that backdrop, near term operating conditions are showing tentative signs of improvement. Seasonal demand recovery, inventory repricing and firmer product prices relative to the first quarter are expected to support sequential margin expansion in April-June. While this does not represent a structural recovery of the petrochemical cycle, it may provide temporary relief to operating cash flow at a critical juncture, reducing immediate financial stress as governance changes take hold. External macro forces are also influencing this short-term window. Escalating tensions between the US and Iran have disrupted global energy flows, increased freight risk and pushed crude prices higher. For petrochemical producers, the effects are mixed. Sustained oil inflation ultimately raises feedstock costs and challenges naphtha-based economics, but initial price movements tend to favor resin producers, as selling prices adjust more rapidly than feedstock benchmarks. This dynamic has supported margins in certain chains, especially for polyethylene (PE) and polypropylene (PP), both Braskem's products, despite broader instability. For Braskem, the overlap of these forces creates a narrow but meaningful corridor. On one side lies the structural necessity of financial and governance reorganization after years of shareholder instability. On the other is the possibility that short-term operating conditions may soften the adjustment, offering incremental breathing space as the new control structure is implemented. The stakes extend beyond the company. As Latin America's largest petrochemical producer, Braskem plays a central role in regional polymer supply, pricing formation and investment signaling. A completed control transition would not only reshape internal governance but could recalibrate expectations across the region's chemical markets, influencing capacity decisions, import dynamics and competitive behavior. Whether this moment marks the beginning of a broader reset or merely a stabilization phase remains uncertain. What is clear is that Braskem has moved beyond regulatory limbo and into a decisive phase where execution, market conditions and geopolitics will jointly determine its trajectory. The coming quarters will reveal whether marginal operating relief can coincide with structural change or whether deeper intervention will still be required. By Fred Fernandes Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Gdansk refinery ups output after maintenance

Gdansk refinery ups output after maintenance

Warsaw, 8 April (Argus) — Poland's 210,000 b/d Gdansk refinery is increasing production after completing scheduled maintenance earlier this month. Most of the units taken off line for between late February and early April have restarted, as planned, operator Rafineria Gdanska said on 7 April. Maintenance was conducted on crude and vacuum distillation units, a diesel hydrotreater, the MHC mild hydrocracker, a reformer, the jet fuel Merox and hydrogen generation units, and two sulphur recovery units. A second phase of planned maintenance at Gdansk takes the refinery's three base oil units off line from 8 April until mid-May. Rafineria Gdanska is a joint venture of state-controlled Orlen with 70pc and state-controlled Saudi Aramco holding 30pc. Orlen is planning maintenance on a hydrocracker at its 373,000 b/d Plock refinery in Poland from 13 May until 24 June. The Polish company's 63,000 b/d Kralupy refinery in the Czech Republic has been shut down for scheduled maintenance since mid-March and should restart in early May. Orlen's 190,000 b/d Mazeikiai refinery in Lithuania was off line for 30 days of planned maintenance last month. By Tomasz Stepien Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.