Weight of Freight: TMX spurs new Aframax, VLCC trade in Pacific basin

The first three months of Canada's Trans Mountain Expansion (TMX) have sent a surge of crude to refiners in California and China, shifting tanker demand in the Pacific basin.

The 590,000 b/d TMX project nearly tripled the capacity of Trans Mountain’s pipeline system to 890,000 b/d when it opened on 1 May, linking Alberta's oil sands to Canada's west coast for direct access to lucrative Pacific Rim markets, where buyers are eager for heavy sour crude.

Between 20 May, when the first TMX cargo began loading, and 20 August, about 165,000 b/d of Vancouver crude exports landed at ports on the US west coast, primarily in California, up from about 30,000 b/d in that same span last year, according to data from analytics firm Kpler.

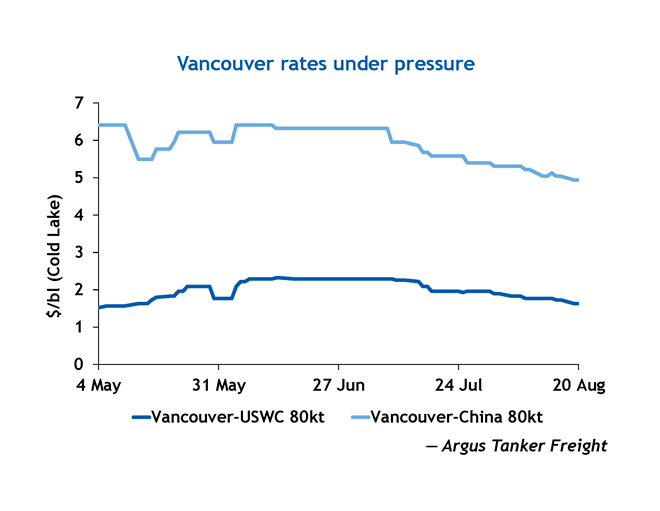

The freight rate for a Vancouver-US west coast Aframax shipment averaged $1.98/bl for Cold Lake between 1 May and 20 August. This ranged from a low of $1.50/bl from 1-3 May when shipowners repositioned to the region in anticipation of TMX to a high of $2.32/bl from 13-14 June, according to Argus data.

The new oil flow into the US west coast has displaced shipments from farther afield in Ecuador and Saudi Arabia. Crude exports from those countries into the US west coast averaged 110,000 b/d and 25,000 b/d, respectively, between 20 May and 20 August, down from 155,000 b/d and 135,000 b/d over the same stretch in 2023, according to Kpler.

The growth of the Vancouver market, which benefits from its proximity to California, has reduced tonne-miles, a proxy for tanker demand, into the US west coast. This has outpaced slightly lower crude demand, which fell in part due to Phillips 66 halting crude runs at its 115,000 b/d refinery in Rodeo, California, in February to produce renewable fuels, as well as weaker-than-expected road fuel demand this summer.

Tonne-miles for US west coast crude imports fell by 14pc to 106bn between 20 May and 20 August 2024 compared with the same period a year earlier, Vortexa data show, while overall crude imports declined just 8.6pc to 1.37mn b/d, according to Kpler.

PAL-ing around with VLCCs

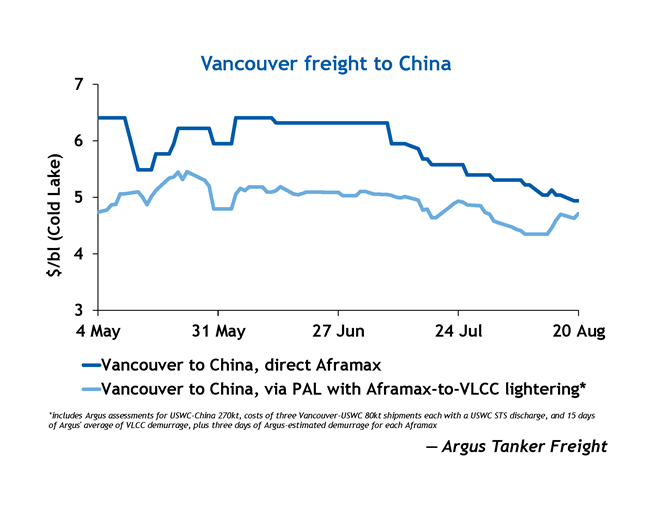

Though much of Vancouver’s exports have been shipped to the US west coast, Canadian producers have found ready buyers in Asia-Pacific as well, where about 160,000 b/d of Vancouver exports went between 20 May and 20 August, compared with none a year prior, Kpler data show.Buyers and sellers have displayed a preference for using ship-to-ship transfers onto very large crude carriers (VLCCs) at the Pacific Area Lightering zone (PAL) off the coast of southern California, rather than sending Aframaxes directly to refineries in east Asia. Of the 30 Vancouver-origin Aframax cargoes that have landed in China, South Korea and India, 19 were transferred onto VLCCs at PAL, Kpler data show. Seven cargoes were sent directly to east Asia on time-chartered Aframaxes — the majority by Suncor — and just four were sent using spot tonnage, likely due to the expensive economics of trans-Pacific Aframax shipments.

The Vancouver-China Aframax rate between 1 May and 20 August averaged $5.90/bl, with a low of $4.94/bl from 19-20 August and a high of $6.41/bl from 1-10 May and again from 4-12 June, according to Argus data.

Over the same time, the cost to reverse lighter, or transfer, three 550,000 bl shipments of Cold Lake crude from Vancouver onto a VLCC at PAL averaged about $8.055mn lumpsum, or $4.92/bl, with a low of $4.35/bl from 8-13 August and a high of $5.45/bl on 22 May, according to Argus data. This includes $150,000 ship-to-ship transfer costs at PAL, 15 days of VLCC demurrage and three days of Aframax demurrage for each reverse lightering.

VLCC costs could change preferences

Though it may have been cheaper to load TMX crude on VLCCs at PAL since May, volatility in the VLCC market — which often falls to yearly lows in summer before climbing to seasonal highs in the winter — could entice traders to opt for direct Aframax shipments if VLCCs hit their expected peak in the winter.

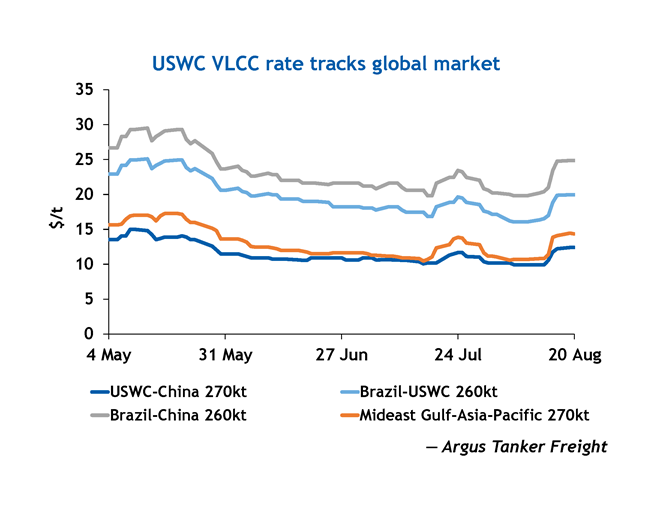

VLCC costs for shipments from the US west coast to China are influenced by the VLCC markets in the Mideast Gulf and Brazil, where ships look for their next voyage after discharging on the US west coast.

For now, Vancouver-loading Aframax rates are under pressure from the reemergence of VLCCs in what had become an Aframax trade in Thailand, boosting Aframax supply in the Pacific and pulling the class’s rate to ship crude from Vancouver to the US west coast to its lowest level in more than three months on 19 August.

In mid-July, VLCCs resumed discharging via single point mooring (SPM) at Thailand's port of Map Ta Phut for the first time since January 2022, ship-tracking data from Vortexa show. Prior to the SPM's return to service, VLCCs could discharge cargoes only by lightering onto smaller Aframaxes, which would then unload at a different berth in the port.

This created demand for about eight Aframax lighterings each month, but with VLCCs in Thailand again able to discharge directly, that demand is effectively halted, putting downward pressure in the broader southeast Asia Aframax market.

Since July, two Aframaxes have left the southeast Asia market for Vancouver, according to ship tracking data from Kpler: the Eagle Brisbane, which previously was used in lightering operations at Map Ta Phut, and the Blue Sea, which recently hauled fuel oil from nearby Singapore to China.

Spotlight content

Related news

Iran war prompts IMF to cut growth outlook

Iran war prompts IMF to cut growth outlook

Washington, 14 April (Argus) — The energy supply shock sparked by the US-Israel war against Iran and the uncertainty over the conflict's duration have forced the IMF to change its quarterly outlook for global economy by outlining scenarios that range from bad to worse. Even with a fragile truce in place through 21 April, "some damage is already done, and the downside risks remain elevated," IMF chief economist Pierre-Olivier Gourinchas said on Tuesday. "The shock's ultimate magnitude will depend on the conflict's duration and scale — and how quickly energy production and shipment normalize once hostilities end." The IMF's World Economic Outlook pegs global growth at 3.1pc in 2026, a downgrade of 0.2 percentage points from its January outlook. The IMF describes this as a "reference forecast", rather than a baseline case, highlighting the unpredictable trajectory of the war. In the reference scenario, disruptions from the shut-in of Mideast Gulf production and the closure of the strait of Hormuz would fade by July. A longer shutdown of the strait of Hormuz and additional damage to Mideast Gulf upstream and refining capacity would result in global growth slowing to 2.5pc this year. In this adverse scenario, oil and gas prices would remain above pre-war levels well into 2027. The most severe scenario analyzed by the IMF, in which oil and gas supply disruption lasts into 2027, would reduce growth this year to 2pc, the IMF said. By Haik Gugarats Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

BP to simplify organisational structure

BP to simplify organisational structure

London, 14 April (Argus) — BP plans to reorganise into a simplified structure with two distinct upstream and downstream segments, the company confirmed today. "In service of becoming a simpler, stronger, more valuable BP, we intend to build an organisation with a clear upstream and downstream," chief executive Meg O'Neill said in a statement to employees. She added she is "committed to providing clear direction and consistency so we can move forward together with confidence". The move follows comments made in late March by BP chairman Albert Manifold, who said the company wants to shift towards simpler, more standardised and more comparable reporting. BP currently reports results across four segments: Gas & Low Carbon Energy; Oil Production & Operations; Customers & Products; and Other Businesses & Corporate. The reorganisation comes as management changes loom at the company's downstream business. BP's Customers & Products head Emma Delaney was nominated last week as the next chief executive of Austrian oil company OMV. Earlier today BP flagged an "exceptional" oil trading performance in the first quarter. But the company said price lags of up to two months meant it failed to capture the full benefit of higher oil and gas prices during the period. BP will publish its first-quarter results on 28 April. By Jon Mainwaring Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

Q&A: Hormuz tensions put spotlight on marine insurance

Q&A: Hormuz tensions put spotlight on marine insurance

Singapore, 14 April (Argus) — As tensions in the Middle East disrupt global shipping routes, insurance has become a critical factor for vessel operators and cargo owners. George Grishin, chairman of UK-registered Lloyd's insurance broker Oakeshott Insurance Group, spoke with Argus on 13 April about how the shipping industry is responding to the announcement of a two-week ceasefire, the insurance options currently available, and the potential long-term implications that the US-Iran war could have for relations between shipowners and insurers. How has the insurance market reacted to the announcement of a two-week ceasefire? The announcement briefly encouraged insurers to return to the market, particularly for quoting war risk cover for vessels transiting high-risk areas, such as the strait of Hormuz. War risk premiums are extremely sensitive to geopolitical developments, and rates can change daily. A ceasefire needs to be stable and verifiable before insurers are willing to reduce prices or expand capacity. What is really happening is that insurers are reassessing risk in real time, and in some cases, they simply cannot accept it. There were reports that insurers withdrew cover entirely during the escalation. Is that accurate? Not exactly. Much of this confusion comes from a misunderstanding of different types of marine insurance. Physical damage to vessels and cargo is covered by hull and machinery (H&M) or war risks insurance. Protection and indemnity insurers (P&I) cover a shipowner's third-party liabilities, not damage to the ship itself. Typical P&I cover includes third-party liabilities, such as crew injury or pollution, for example. War risk insurance for physical damage has remained available in many cases, but often at a higher cost and with tighter conditions. How does war risk insurance work when a region is classified as high-risk? Once an area is listed by the Joint War Committee (JWC), war risk cover for calls in that area is automatically excluded. Shipowners or cargo owners then have to buy additional cover for specific voyages or periods, typically priced as a percentage of the vessel or cargo value and valid for just seven days. This applies to ports as well as sea passages. The most recent expansion of the listed areas prior to the current escalation took place in December 2023, when Guyana was added. The list was subsequently updated on 3 March 2026, with the inclusion of several countries that had not appeared on it for many years — Bahrain, Djibouti, Kuwait, Oman and Qatar. At the same time, the geographical scope was widened to cover parts of the Persian/Arabian Gulf, the Gulf of Oman, parts of the Indian Ocean, the Gulf of Aden and the southern Red Sea. What kind of costs are shipowners facing today? Additional war risks premium (AWRP) levels for tankers and bulk carriers stood at around 1pc on 13 April with a 35–50pc no claim bonus (NCB) applied to vessels remaining in the Mideast Gulf. NCB is a discount given by insurers if no claim is made during the period of cover. AWRPs for H&M in the Gulf of Oman and in the Bab el-Mandeb strait were reported at around 0.5pc and 0.75pc, respectively. Passage through the strait of Hormuz is considerably more complex. At one point during the ceasefire discussions, insurers quoted around 3pc of value for a single passage for a seven-day period on 10 April, but those quotes were quickly withdrawn. Why is the strait of Hormuz particularly difficult to insure? The probability of an incident is simply too high, especially for vessels carrying oil or gas. Insurers have to price risk based on probability, and in some scenarios the likelihood of a vessel being hit could be extremely high. Charging higher premiums of, for example, 25–50pc of vessel value would theoretically reflect that risk, but such rates are commercially unviable, no shipowner could afford them. In those cases, insurers may refuse to quote altogether. Are all vessels treated the same from an insurance perspective? No. Flag, ownership, and cargo type matter enormously. Indian- and Chinese-flagged vessels have faced fewer restrictions in recent weeks, and container ships and bulk carriers are generally seen as lower-risk than tankers. Insurers also scrutinise ultimate beneficial ownership (UBO) and compliance very carefully before offering cover. Why do some owners still insure vessels that are stuck in port? This is where the London Blocking and Trapping Addendum becomes important. It extends war risk cover to situations where a vessel is unable to leave a port or waterway for a continuous agreed period, typically six or 12 months, due to war-related closure. If that period is exceeded, the vessel can be treated as a total loss, even without physical damage. Does blocking and trapping insurance require a separate policy? No. It is an extension of existing war risk cover. It costs more, but it protects against long-term immobilisation rather than just physical damage. This type of cover proved crucial for vessels trapped, for example, in Ukrainian ports in 2022–23, where some owners eventually received full compensation for their ships. Could recent events change the relationship between shipowners and insurers? Yes. Trust has been strained, particularly when owners see insurance becoming unavailable just when they need it most. But insurers face their own constraints — they cannot price risk at levels that are mathematically accurate but commercially impossible. The long-term challenge will be finding a sustainable balance between affordability and realistic risk pricing in an increasingly unstable geopolitical environment. What needs to happen for insurance conditions to improve? Time and clarity. Insurers need a longer observation period to assess whether a ceasefire is genuinely holding. Only then will premiums stabilise and capacity return. Until that happens, insurance will remain costly, selective, and highly conditional. By Anna Cherkizova Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.

IEA warns Hormuz oil export recovery will take months

IEA warns Hormuz oil export recovery will take months

London, 14 April (Argus) — Oil exports through the strait of Hormuz are likely to take around two months to stabilise once the waterway reopens, the IEA estimates. Disruptions to shipments through the strait due to the US-Iran war have forced producers in the Mideast Gulf to shut in part of their output because of limited alternative export routes. The IEA estimates that the shut-ins cut global oil supply by 10.1mn b/d in March and forecasts a further 2.9mn b/d decline in April. A sustained recovery in production depends on restoring exports through Hormuz. Laden tankers would first need to exit the Gulf, after which empty vessels inside the waterway would load cargoes and draw down stocks, the IEA said. "It will be impossible to start upstream production or refining unless there is a foreseeable loading programme with adequate available storage at ports," the IEA said. Tanker availability could slow that process. Around 390 vessels, including 210 laden tankers, were trapped in the strait when the conflict began on 28 February, the IEA said. Since then, a net 49 tankers have exited. Many ballast tankers waiting outside Hormuz have since moved to other markets, meaning it could take longer for ships to return to pick up the first cargoes once exports resume, the agency added. Iraq may face particular difficulties in restarting exports quickly because of limited storage capacity at its ports. Upstream constraints could further delay a production recovery. Half of Mideast Gulf oil fields have "sufficient reservoir pressure and fluid characteristics" to return to pre-war output within about two weeks once exports resume, rising to 80pc after roughly one month, the IEA said. The remaining 20pc may prove harder to restart because of issues such as "pressure depletion or flow impairment from wax or asphaltene deposition". Many of these more complex fields are in Iraq and Kuwait, the agency said, adding that some lost pre-war production may not return. "Some fields may require specialised oil field services, including workovers, coiled-tubing units, chemical treatments or perforation," the IEA said. Fields relying on secondary or enhanced oil recovery could face longer restart times because they depend on uninterrupted supplies of gas, power, steam and chemicals, the agency added. By Aydin Calik Opec+ crude production declines 'mn b/d Mar Feb Mar vs Feb Saudi Arabia 7.25 10.40 -3.15 Iraq 1.57 4.57 -3.00 Kuwait 1.19 2.54 -1.35 UAE 2.37 3.64 -1.27 Bahrain 0.04 0.18 -0.14 Iran 3.63 3.69 -0.06 source: IEA Send comments and request more information at feedback@argusmedia.com Copyright © 2026. Argus Media group . All rights reserved.